Commercial Insurance Price Growth Slows to 2.5% in Q1 2026

U.S. commercial insurance buyers saw price increases continue to moderate in the first quarter of 2026, with aggregate pricing rising just 2.5% compared with the same period a year earlier, according to WTW’s Commercial Lines Insurance Pricing Survey (CLIPS).

The survey measured prices charged on policies underwritten in Q1 2026 against those charged for the same coverage in Q1 2025. The CLIPS data is drawn from prices reported by carriers, according to WTW.

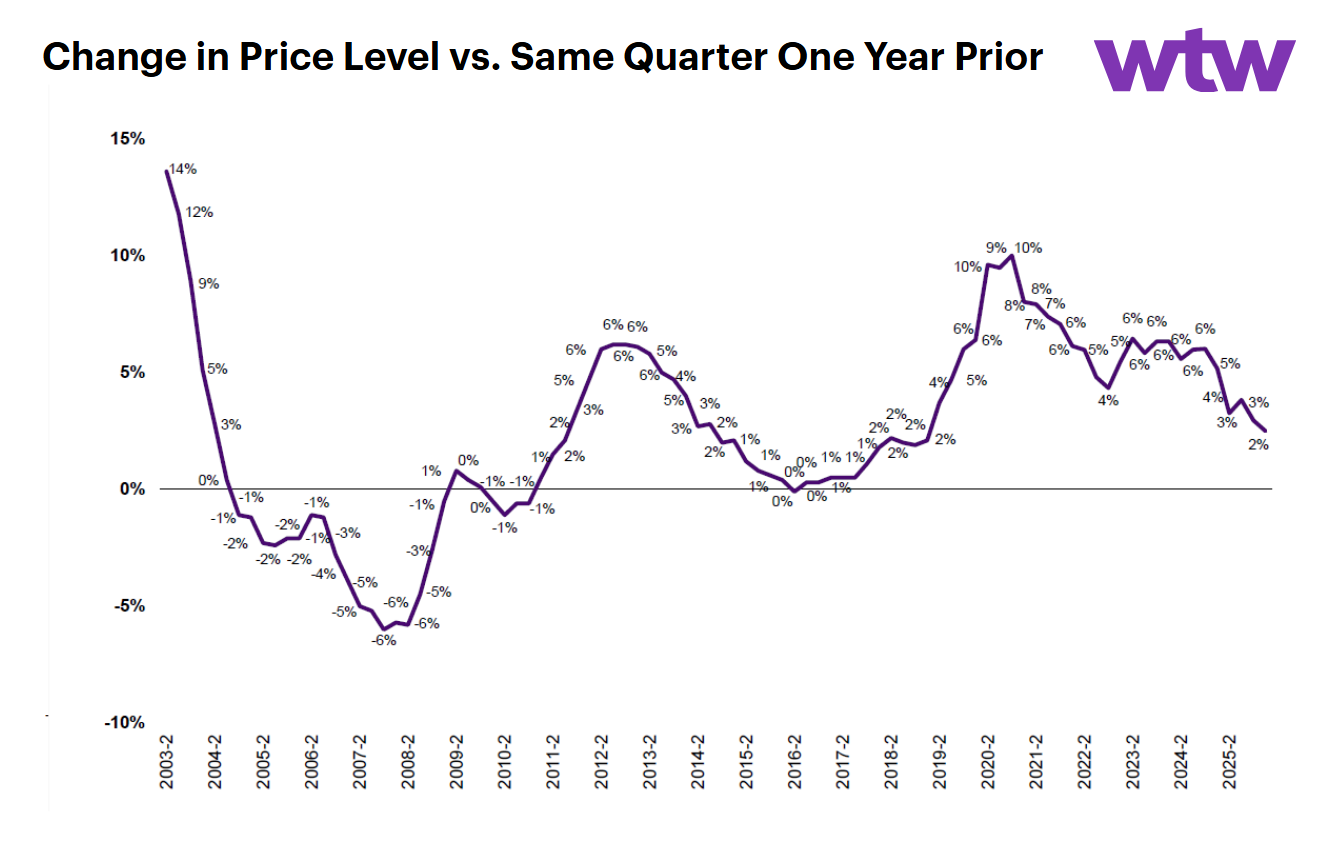

The trajectory of commercial pricing over the past several years shows a market that surged, stabilized at elevated levels, and has now moved into a notable period of deceleration, WTW said. After spiking to nearly 10% aggregate increases in mid-to-late 2020, price growth gradually declined to just below 5% by the fourth quarter of 2022, according to WTW. A brief reversal pushed increases above 6% in the second quarter of 2023, and pricing held around that level through early 2025. Since then, the survey found, price growth has dropped, landing at 2.5% in the most recent quarter.

WTW Commercial Lines Insurance Pricing Survey (CLIPS) Q1 2026

Line-by-Line Trends Vary Widely

The softer aggregate figure masks significant variation across individual lines of coverage, WTW noted. Workers’ compensation, directors’ and officers’ (D&O) liability, commercial property, and cyber were the exceptions to the moderate to significant price increases reported across most other surveyed lines in Q1 2026, according to WTW. Most other lines posted similar or lower increases compared with the prior quarter.

Excess and umbrella liability continued to post the largest price increases among all surveyed lines, the report said. Commercial auto, a line that has faced sustained upward pressure on pricing, recorded its first sub-double-digit price increase since the third quarter of 2023, according to WTW.

Commercial property, which experienced significant price increases through 2023, has seen a notable reversal. The line recorded its first price decrease in the second quarter of 2025, and that downward pressure has continued through Q1 2026, following several quarters of progressively moderating increases.

Account Size and Specialty Pricing

Across all account sizes, reported price increases in Q1 2026 were slightly lower than in the prior quarter, according to the survey.

The interplay between professional liability and D&O remained a defining dynamic within specialty lines. Professional liability continued to generate positive price movement, while D&O recorded a price decrease, the survey found. Specialty lines overall posted a small aggregate price increase as a result of the professional liability price increase offsetting the D&O price decrease, according to WTW.

View the full report here. &