Risk Insider: Nir Kossovsky

VW’s Reputation Crisis Likely to End Badly

Nir Kossovsky is CEO of Steel City Re, which mitigates the hazards of reputation risk with parametric reputation insurances, ESG insurances, and risk management advisory services.

One of the many lessons to emerge from studies of reputation is the importance of governance in protecting enterprise value.

A gut appreciation of this role is one of the reasons corporate boards have named reputation risk to be their top concern. Hard numbers may compel them to move beyond mere concern to material action.

Stakeholders expect behaviors from corporations just as they expect them from persons. And in the eyes of stakeholders, corporations can be held to behavioral standards.

That’s why the disclosure that Volkswagen executives intentionally deceived regulators will probably have long-term, substantial consequences.

While courts of law may not send corporations to jail for criminal offenses, courts of public opinion — read, stakeholders — may jail them figuratively for a variety of offenses that impact reputation: ethics, innovation, quality, safety, sustainability and security.

The common thread for all six of these offenses is gross disappointment, the progenitor of reputation damage.

If corporations are persons, then their directors and officers are their brains. Over the past few years, two other major automobile manufacturers, in addition to Volkswagen, experienced adverse events that looked like reputational crises, and for which their executives received public opprobrium.

Toyota had a safety issue with its accelerator pedal; General Motors had a problem with its ignition key design.

If corporations are persons, then their directors and officers are their brains.

Volkswagen now has an issue with its engine emissions. Of the three, ethics and questions of governance, willful ignorance, or even overt misbehavior have been most strongly associated with GM and VW.

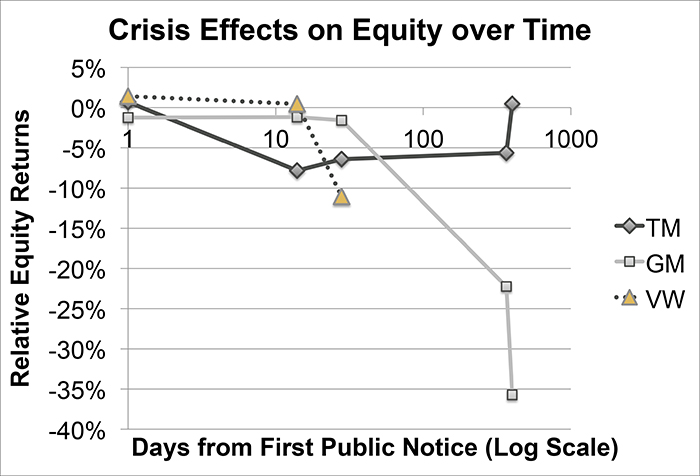

Using an economic loss model, we looked at the short- and long-term economic costs to Toyota, GM, and VW. Given the size and global nature of the three giant manufacturers, we measured their period gains and losses relative to the performance of a basket of equity indices: Nikkei 225, DAX, and S&P500.

On average, Toyota underperformed by 8 percent within the first two weeks of its serial notices of brake issues in 2010; underperformed by only 6 percent one month out, underperformed still 6 percent one year out, but had accelerated and caught up with the world markets by around 13-14 months. Bottom line: no persistent reputation damage.

GM’s trajectory was slower to launch with only a 2 percent underperformance at one month. But as equity investors studied the broad implications, by one year from the first public disclosures GM had underperformed over the trailing 12 months by 22 percent and by 13-14 months out, underperformed by 36 percent.

Bottom line: the suggestion that a long-term cover-up was sanctioned by some level of management led to material enterprise-level reputation damage.

The VW story is still evolving, and the suggestion is that some level of management is culpable. At an average of one month out from serial public disclosures, VW is underperforming the basket of equity markets by 11 percent, suggesting its long-term course will be more like GM than Toyota. (See figure.)

This costly lesson affirms the general principle that stakeholders will forgive point failures like an errant supplier for Toyota, or even a London Whale for JPMorgan Chase.

They will be less forgiving if the shortcoming appears to be evidence of a systemic failure engineered by directors and officers.