Rising Hail Damage Costs Are Rattling the Solar Industry — Luckily, Parametric Solutions Are on the Case

The topic of climate change and what we can do to confront it has never been more top-of-mind — so it’s no wonder that solar power is growing in popularity. New real estate development calls for new sources of energy, and the push is on for more renewables. According to the U.S Energy Information Administration, the first nine months of 2023 saw the installation of a record 15.8 GWac of photovoltaic capacity, an increase of 31% over the previous year.

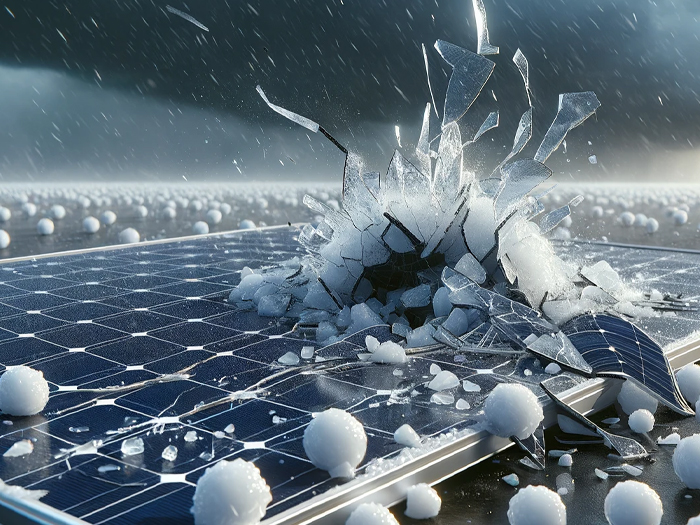

At the same time, hailstorms have been growing more severe, and quite often in regions that are otherwise seen as prime locations for solar farms. Solar panels, though, are more vulnerable to hail damage than most other categories of property; large hailstones can shatter solar panels, and even smaller hail can create “invisible” damage that allows panels to continue functioning but with reduced effectiveness, producing less electricity and generating less revenue.

In 2023, the combination of changing weather patterns and growing development in new geographies resulted in the P&C market’s worst year in a decade. Despite last year’s relatively tame hurricane season, the U.S. witnessed more $1 billion-plus weather events than we’ve ever seen — of the 28, 17 were severe weather and hail events.

A recent CoreLogic report found that this convergence of increased solar capacity and more severe hailstorms is especially pronounced in Texas, the Southeast and the Plains. The report depicts a clear rising trend in the number of days of hail over 2″ in diameter each year — and last year was a particularly active one. In 2023, Louisiana saw 65% more days with 1″ hailstones compared to the 20-year trend, Tennessee 60%, Alabama 54% and New Mexico 45%.

With 42% more days of 1″ hail in 2023 than average, Texas was not far behind — and Texas is an important market all on its own. Not only is it on its own grid (ERCOT, which generates more than 12% of the nation’s total electricity and consumes more energy than any other state), but it’s also one of three states that account for the lion’s share of new solar panel installations: In 2023, 11% of new installations and 20% of new deployments were in Texas. Together, California and Texas account for 62% of the country’s grid-scale installations.

A GCube report from late last year confirms that the effect of these intersecting trends is already being felt: Hail is now responsible for more than half of all solar claims costs, despite constituting only a fraction of solar claims by volume. The average solar hail claim now comes to a whopping $58.4 million. And insurers are feeling the pinch: In 2023, The New York Times reported, State Farm’s hail claims totaled over $6 billion — more than the previous two years combined.

If there’s one thing that’s true of hail, it’s that what goes up must come down. Can the same be said of its harmful effects? Is it possible to manage the risk of solar losses due to hail and reverse this worrying trend?

Supply & Demand

Risk & Insurance recently spoke with Brenden Beeg, business development manager, North America, Descartes Insurance (a parametric insurance provider specializing in modelling climate and emerging risks that offers parametric solutions against hail risk), and Brendan Fountain, vice president, energy & marine, Alliant Insurance Services (a broker who has placed these policies in the past).

As Fountain explained, the cost to replace damaged solar projects has gone up due to inflation in general, the tight labor market, and supply chain issues related to the increased overall growth of solar described above.

Brendan Fountain, vice president, energy & marine, Alliant

“There’s a tremendous amount of investment-supported administration policy to build out these projects,” Fountain said. “For example, the IRA [Inflation Reduction Act] extension of the tax credits for renewable energy generation includes adders for both domestic content and domestic labor to qualify some of these overall credits.”

Fountain continued, “If we’re talking about supply chain and inflationary concerns, it then comes down to how many project owners and developers are looking to satisfy domestic requirements within the IRA, and how much does that create congestion for project owners in the supply chain? And then, like anything else, finding the labor to support the demand for new projects — no matter the industry, there’s always a question of the availability of experienced labor.”

A rising cost to replace swiftly translates into rising cost to insure. And for all our green energy ambitions, this leaves both insurers and insureds in a difficult spot.

“Solar underwriters continuously monitor their exposure aggregations, especially in states like Texas or Colorado, where there can be a large concentration of risk,” Beeg said.

“Going back to the hard market, there was a significant demand and supply imbalance. Asset owners are required to carry a certain amount of insurance coverage for these Nat CAT perils, so the imbalance has led to challenges for both the asset owners and the underwriting side of things. For underwriters, it goes back into the reinsurance market; to monitor those aggregations, there needs to be additional reinsurance capacity available, and potentially, there’s just not the capacity available in certain situations.”

Product manufacturers, risk engineers, the IBHS and others are hard at work to develop more robust solar panels, new ways of protecting them from hail, and improved best practices for their installation, deployment and stowing — all in an effort to cut down on future losses. In time, we can expect new methods of loss avoidance to bear fruit.

Meanwhile, power project owners can work closely with their original equipment manufacturers to understand the tolerances of their products and what they can do to preserve their integrity — and they can watch the skies.

But even with their solar arrays installed and maintained according to current best practices, owners looking to protect these assets will continue to depend heavily on risk transfer for the foreseeable future.

Bespoke Coverage

With the demand for coverage high and costs rising, parametric covers give solar project owners struggling to find insurance some additional options.

“It’s no secret that the general property market is looking to impose increased deductibles, lower sublimits and increase premiums for projects that are located in areas prone to natural catastrophic events,” Fountain said. “So it becomes the responsibility of brokers to conduct significant due diligence for the benefit of our clients, to really understand their inherent risk and how, from a technology perspective, our clients have mitigated that risk. From there, we can engage the insurance market to develop effective solutions.”

He added that the benefit of a parametric policy is that it has “the ability to tailor coverage off very specifically designed and agreed-upon policy triggers — namely, hailstone size.”

Solar owners can thus determine what size of hailstone their panels can withstand, calculate the probability that future hail will exceed that size, conclude how much risk they want to retain, and then very precisely make up the difference between that retention and a general P&C policy.

“Ultimately, it gives us a high level of specificity with how we can tailor the coverage,” Fountain said, “and in a way that matches the project characteristics … We can implement the coverage to essentially buy down deductibles that you may find in a typical property policy, or we can replace a policy sublimit. Ultimately, it comes down to each and every client’s specific risk tolerance.”

Fast & Easy

Parametric hail covers have another advantage over general P&C: Settling claims is far simpler and faster.

Brenden Beeg, business development manager, North America, Descartes Insurance Solutions

“It’s based on radar imagery,” Beeg said of how insurers determine whether a policy has been triggered. “The U.S. has good radar infrastructure; there are Doppler radars networked throughout the country, and we work with third-party data providers that accurately certify that data. We’re able to look at, in quite granular views, the hail swath or the hail track of an event and see what hailstone sizes were falling, and we can see what area of the asset was impacted.”

This alone can help businesses to keep their bottom line in check. “It’s objective in nature; everything is extremely transparent, so from a budgeting perspective, it’s a little bit easier to anticipate,” Beeg added.

“And then when it comes down to an actual claim event, from the point of a triggering event to the money actually flowing, you’re looking at within about a 30-day window,” Beeg said. “This is a completely different scenario compared to the traditional indemnity markets, which oftentimes go through extremely detailed forensic adjustments or other types of processes … Depending on the class of business, it could be outside of a year before a [traditional] claim is fully adjudicated.”

Finally, Beeg said, “another key benefit of parametric insurance is that it doesn’t have to adhere to physical damage or business interruption. The limit at risk is essentially all in terms of economic damage, so really anything that could be sublimited, wherever there’s gaps or there’s exclusionary wording on the traditional side of things, parametric payouts can be utilized to offset or take up that economic damage burden. There’s a lot of flexibility. There’s a lot of transparency. And then there’s just overall speed and liquidity.”

Ultimately, Fountain added, almost everyone wants to see solar succeed, so rather than keeping their insight into how to protect projects to themselves, stakeholders have a tendency to share information freely.

“It’s a growing sector,” Fountain said. “There’s a tremendous amount of government policy driving investment into renewables. Generally speaking, a lot of what we’re talking about here are alternative solutions to support our clients’ projects — whether it’s engineering recommendations to improve project performance in these natural catastrophe-prone regions or alternative risk solutions such as parametrics. The willingness to share this impactful information can only help our clients optimize their projects. [As brokers,] we’re always trying to find ways to align our clients with good partners such as Descartes and other insurers who support that goal.” &