Specialty Insurance

Reauthorization Looms for NFIP, Calls for Greater Private Sector Involvement

In November, the U.S. House of Representatives voted to revamp the National Flood Insurance Program (NFIP).

While the Senate isn’t expected to pass its own revised version until sometime in 2018, the House version calls for greater private sector involvement in the writing of flood insurance and penalties for owners whose properties are the site of repeat flood claims.

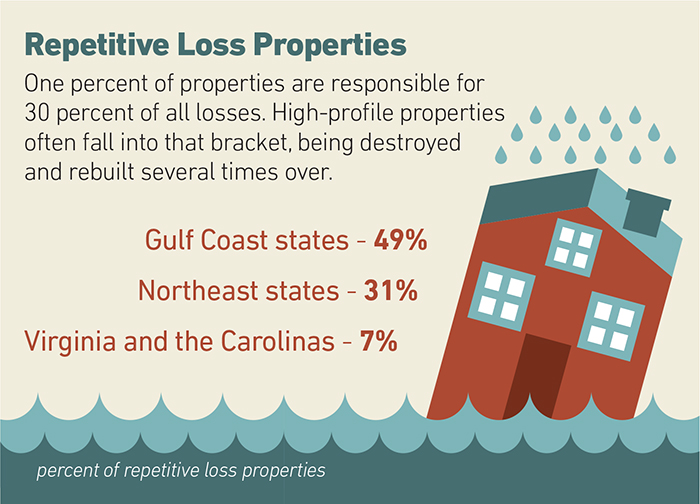

By one estimate, one percent of properties are responsible for 30 percent of all NFIP losses. Private insurers have long complained about a lack of transparency in pricing and transferring risk under the Federal program, which was founded some 50 years ago, because private sector insurers were unwilling to take on the risk.

Since the onslaught of Hurricanes Katrina and Rita in 2005, the program has struggled with debt. Congress in October forgave $16 billion in NFIP debt in an attempt to maintain the program in some state of viability.

According to Daniel Alpay, line underwriter, flood and household, Hiscox, the current situation with the NFIP is not dissimilar to the issues faced by the Terrorism Risk Insurance Act, another federally-backed insurance program.

“Both required reform, and both have experienced delays to reform with short-term extensions,” he said.

“We saw a few NFIP lapses and short-term extensions between 2008 and 2012, which led to mortgage market disruption and lenders demanding owners buy flood coverage for homes in high-risk areas, before the NFIP was finally re-authorized.”

Alpay added, “It’s anyone’s guess as to what will happen, but I would say it’s very possible that something similar [to what has happened before with NFIP] could happen again if there is still polarization in Congress.”

Access to Affordable Insurance

“Either way, consumers need clarity and access to affordable flood coverage as recent events have sadly highlighted,” he said. “There are too many consumers in the U.S. at risk of flood who are either not being adequately insured or else not being covered at all.”

Daniel Alpay, line underwriter, flood and household, Hiscox

Achieving bipartisan support is challenging, “but at the end of the day, U.S. citizens need to have sufficient access to affordable flood insurance,” Alpay said.

“The NFIP has played an important part in offering flood coverage to U.S. homeowners and businesses, but it is not sufficient on its own. It requires reform; it is no longer the self-sufficient insurance program that it was set up to be, given it is $25 billion plus in debt.”

Neal Conolly, now a director at ratings company Clearsurance, was the president of Wright Flood, the largest underwriter in the NFIP, until last year. He noted the October $16 billion loan forgiveness by Congress. That relief, plus a $22 billion line of credit at the Treasury, means there is “no financial issue continuing for NFIP.”

“Historically, the program was in balance for most of its 40 years of existence,” said Conolly.

“It was two storms, $17 billion of insured losses from Katrina and $7 billion from Sandy” that put the program under water.

He added that preliminary figures from Harvey will surpass Sandy with $10 billion in insured losses. Irma will be smaller at about $3 billion.

As important as those losses are, Conolly stressed a much larger point: “Coastal development generates half a trillion dollars in economic activity.”

That important economic engine would falter if the program were to be sharply curtailed. Instead he expects NFIP to be tweaked.

However, recent events “confirm that the U.S. flood risk is greater than the NFIP currently caters for or has the appetite to cater for,” said Alpay.

Public-Private Partnerships

“I don’t believe it can continue in its current form, but I do believe there is a role for the private flood insurance market. There are lots of examples where the public and private sectors have worked together, and this issue is too important for us not to.

“Flood is the most frequent natural disaster in the U.S., yet sadly 95 percent of all residential properties are currently uninsured.”

In the past, flood was considered an uninsurable risk for private market insurers, but that may not be the case anymore thanks to improved modeling granularity, computational power and higher-resolution data.

Alpay said Hiscox has invested heavily in understanding and pricing U.S. flood, which is an extremely data-driven process.

“We have built a suite of flood insurance and reinsurance provisions,” he said.

“We have worked with independent hydrological model specialists, [and used] global imaging satellites and remote sensing experts to develop the underwriting platform. It has been peer-reviewed and approved by independent actuarial consultants.”

That said, private insurers such as Hiscox are not involved directly in efforts to reform the NFIP. Those are being led by political and academic groups.

“What we are doing is helping to raise awareness among consumers of the flood risk in so-called non-mandatory flood zones,” said Alpay. Several public policy associations have published analyses and position papers on NFIP reform, including the American Academy of Actuaries (AAA) and the National Association of Insurance Commissioners.

“NFIP is more than just profit and loss. It affects building codes, land use, mapping and funding.” — Rade Musulin, vice president of casualty, AAA

Rade Musulin, vice president of casualty, AAA said, “The program clearly has seen some problems, but NFIP is more than just profit and loss. It affects building codes, land use, mapping and funding.”

Climate change has become the major new variable in the equation, and Musulin does not dispute that.

Modern Risk Assessing Technologies

He hastened to add, “the key point to remember is that the technology around assessing risk is changing rapidly. That is what is opening opportunities for the private sector and is a key driver for revisiting the program. There were many strong reasons it was formed in the ’60s. But now we have CAT models, GPS mapping and big data. Flood risk may have been underestimated in some areas.”

Advances in technology make underwriting and pricing risk more accurate and thus more palatable to the private sector.

“There are some provisions in the reform proposals that direct NFIP to release data,” said Todd Kozikowski, co-founder and chief revenue officer, Clearsurance.

“That includes loss data. NFIP has resisted this because the fear is that the private sector will cherry-pick the best or mispriced risks.”

He added that this is likely to happen to some degree, but the greater good of the competition will be a better differentiation of the risks, including inland from coastal.

Other sources have even suggested that the private sector cherry-picking the best business will then force higher deductions and premiums on the repetitive loss properties. Thus, either enforcing proper pricing on the risk or driving those properties out of the program.

The other technological development being brought to bear is crowdsourcing reviews. Whether properties are FIP or privately insured, Kozikowski said,

“The mission is for insureds to make smarter decisions. We found that legacy reviews were 70 to 80 percent negative, which means they were not really helpful. People only reviewed when they had a complaint. Since we started our reviews, the same percentages are now positive.”

Carriers and brokers pay for granular Clearsurance surveys; insureds do not pay to make reviews. &