Toxic Releases from Floods Spell Higher Insurance Premiums

Hurricanes used to be mostly a coastal phenomenon; high winds and storm surge were the primary hazards. But the last few major storms did most of their damage many miles inland and primarily from days of heavy rain.

The changing nature of natural catastrophes is starting to effect change in environmental liability. The segment has had ample capacity for years. Terms and conditions have not been restrictive. Now carriers say they are re-evaluating their books of business, and brokers say some placements and renewals are a little tougher.

Refineries and chemical plants on the Gulf Coast came through Hurricane Harvey in August 2017 relatively well. But a chemical plant well inland suffered a complete power loss, fire and toxic release. The company, its CEO and the plant manager are now under indictment.

In late August and early September 2018, heavy rains from Hurricane Florence caused overflows and failures of pits storing coal ash at power plants and animal waste at feeding facilities in the Carolinas.

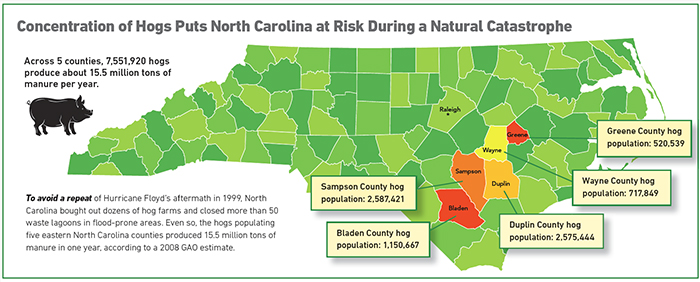

The New Yorker ran an article “Could Smithfield Foods Have Prevented the ‘Rivers of Hog Waste’ in North Carolina After Florence?” in its September 30 issue.

“I was surprised to find hog waste featured in a general interest publication like The New Yorker,” said William McElroy, global head of environmental at Aspen Insurance.

“That shows there is a reasonable public concern about the pollution from industrial sites after a natural disaster.”

Beyond chemical plants, ash pits and waste lagoons, “I would add to that solid-waste facilities and fuel storage and distribution centers,” said McElroy. “In a flood, windstorm or earthquake, a release of major pollutants is always possible.”

There has long been public call for ash pits and hog lagoons to be phased out, but those industries have powerful lobbying efforts against regulatory and legislative restrictions. By contrast, the insurance sector is already taking action.

“There has certainly been an apparent abundance of capacity in environmental liability,” said Chris Smy, managing director and global environmental practice leader for Marsh.

“That is especially true of new entrants that can price aggressively, because they do not have to contend with the incurred but not reported losses that established carriers have. In every segment there will always be a market out of the brackets of other markets.”

“While it may appear that the market is not responding to the frequency of these events, there may be movement behind the scenes in terms of rates and attachment points that would not be evident to outside parties.” — William McElroy, global head of environmental, Aspen Insurance

There is also the lagging effect of multi-year programs common in environmental liability. “We absolutely do see the capacity issue being addressed,” said Smy. “I am dealing with one right now.”

He explained that a “bifurcation” of the market is developing. “For the less-hazardous facilities and shorter terms, there is still ample capacity. For those with CAT exposure, the market is much more challenging.

“It is definitely reacting to these events, and we as brokers are having to work harder. We are having to layer programs rather than place with one carrier with a large limit. Carriers are re-evaluating, altering, and even declining.”

Greg Schilz, EVP, JLT Specialty

McElroy, at Aspen, concurred. “While it may appear that the market is not responding to the frequency of these events, there may be movement behind the scenes in terms of rates and attachment points that would not be evident to outside parties.

“Capacity has grown consistently for several years. In any market where there has been such an expansion, there could be a correction, and there are areas of environmental coverage that could benefit from some change.”

Colony Specialty does write some of these risks but stays away from hog lagoons, said Kelly Killimett, vice president and head of environmental.

“From a risk management standpoint, we are starting to see carriers being smarter with their capacity,” she noted. “Lowering limits might cost the purchaser more.”

That said, Killimett added, “Environmental liability is all over the place. We have more than 50 carriers. Each has its own form. Forms for a coal-fired power plant or concentrated animal feeding operation will vary significantly. For a car dealership [in contrast] there may only be on-site liability.”

That reveals the elusive nature of heavy flooding: A car dealership with a few hundred vehicles, each with a 30-gallon fuel tank, suddenly becomes a 10,000-gallon leak of gasoline and diesel oil that can float and spread for miles into residential and agricultural areas.

Still, “many operators don’t buy environmental insurance,” said Gregory Schilz, executive vice president for the environmental practice at JLT Specialty.

“I don’t want to say that we have reached a tipping point, but these natural catastrophes are starting to show not just severity but now regularity as well.”

Until recently, environmental liability was a matter of severity, not frequency. Now it is both, Schilz noted.

“Some markets have not quite caught up with that reality. But some insureds are starting to realize that they need coverage and that it is available.”

Some suggest frequency and severity are not such new phenomena. “In Hurricane Floyd in 1999, dozens of hog lagoons flooded,” noted Geoff Gisler, senior attorney with the Southern Environmental Law Center.

“There was a movement to buy out the feeding facilities.” But that effort petered out.

“There was a notion that Floyd was an unusual event,” Gisler said dryly.

“Then we had Hurricane Matthew two years ago and saw many of the same problems. And now Florence. These are not one-off events, and the risk of flooding is not just in flood plains. The ability of industry to sidestep responsibility for ensuring their waste does not contaminate neighboring property creates a new risk for facilities as storms increase in frequency.”

There are several lawsuits active in North Carolina, and there is criminal prosecution in Texas. On August 3 a grand jury in Harris County indicted French chemical company Arkema, its CEO and a plant manager. The grand jury concluded they were responsible for the release of a toxic cloud over Crosby during Hurricane Harvey.

“Companies don’t make decisions, people do,” Harris County District Attorney Kim Ogg said.

“Responsibility for pursuing profit over the health of innocent people rests with the leadership of Arkema. Indictments against corporations are rare. Those who poison our environment will be prosecuted when the evidence justifies it.”

“We can put together hundreds of millions in limits. The market is 40 years old, and a lot of engineering has been done. Things are getting more technical, and carriers are asking better questions.” — Greg Schilz, EVP, JLT Specialty

The indictment charges they all had a role in “recklessly” releasing chemicals into the air, placing residents and first responders at risk of serious bodily injury. The charge carries penalties of up to five years in prison for the persons and up to a $1 million fine for the corporation.

According to the U.S. Chemical Safety and Hazard Investigation Board (CSB) report, Arkema had multiple safety systems in place to ensure that organic peroxides were kept cold. However, CSB’s May 2018 documentary video of the incident shows primary and emergency generators and electrical equipment at or near ground level.

“All of these layers of protection failed during Hurricane Harvey because of flooding, which was a common mode of failure,” said the report. “None of Arkema’s safeguards used to address electrical power failure met company or industry standards for analyzing independent protection layers for Harvey-level flooding.

“The same floodwater that caused the facility to lose electrical power also compromised the backup emergency generators, the liquid nitrogen system and the refrigerated trailers used to temporarily store and cool the organic peroxide products. Companies need to ensure there are not common modes of failure in their layers of protection.”

Most underwriters offer support in that effort, and the market is healthy, said Schilz. “We can put together hundreds of millions in limits. The market is 40 years old, and a lot of engineering has been done. Things are getting more technical, and carriers are asking better questions.”

Some industries, notably energy, are becoming sophisticated about coverage as well. “We are doing more work in energy than ever,” said Schilz.

“There are lots of transactions, and often the new investors don’t know about the environmental liability. They are buying pollution cover just as a part of the deal. That can be less than half of one percent of the value of the transaction.” &