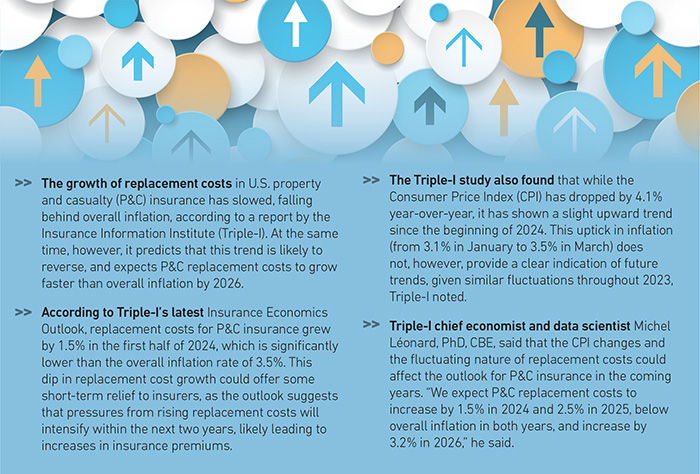

Inflation and Supply Chain Disruptions Increase Replacement Costs, Leading to Underinsurance

Sridhar Manyem, senior director, industry research, AM Best

Replacement costs have soared across the board in recent years as inflation has continued to climb, driven by depressed interest rates.

At the same time, businesses have had to contend with rising labor, fuel and transportation costs to move materials.

Widespread supply chain disruption caused by the COVID-19 pandemic, the conflicts in Ukraine and the Middle East and the collapse of Baltimore’s Key Bridge have further escalated costs.

Added to that has been the cost of damage caused by natural catastrophes, which have become ever more frequent and severe due to the impact of climate change.

As all these economic factors converge, the rebuilding and replacement costs of buildings, fixtures, equipment and vehicles have been driven ever higher.

This is evidenced by the fact that, according to industry estimates, on average, construction material prices increased 12.5% between 2021 and 2023. Vehicle repair costs surged by 23% between January 2022 and January 2023, per the U.S. Bureau of Labor Statistics.

That’s why it’s critical for brokers and underwriters to understand current economic conditions and the macroeconomic risk factors that influence them. They must not only understand them; they must be ready to communicate them to their clients clearly — and as early as possible — in order to build a strong long-term relationship with them and be in a better position to help them should the worst happen.

“If brokers and underwriters understand emerging macro and climate-related trends and are able to explain the factors behind changes in terms and pricing to clients, it will enhance transparency to policyholders and carriers,” said Sridhar Manyem, senior director, industry research at AM Best.

“Educating policyholders about gaps in insurance policies, what is covered and what is not, explaining terms such as cash value versus replacement value and keeping policies up to date so insured values are accurate will minimize surprises when losses happen.”

Inflationary Pressure

Jill Dalton, managing director, U.S. property risk consulting group, Aon

Inflation has had the biggest impact on replacement costs. It started with supply chain problems caused by the pandemic and has been exacerbated by labor shortages, increased consumer demand and global conflict.

“Clients are still wrestling with the fact that the insurable replacement cost in the event of a loss would be significantly greater today than it would have been in 2019 or 2020, pre-COVID,” said Tim Ramsayer, valuation practice leader at Marsh. “That’s across the board, in terms of construction materials and equipment and labor.”

Brokers and underwriters can stay abreast of current macroeconomic conditions by regularly monitoring the latest economic indicators and forecasts. And by updating input parameters for underwriting models in a timely fashion, they can ensure they’re as accurate as possible.

“It’s important for brokers and underwriters to review current economic data as it pertains to construction material and labor costs, as well as to inflation forecasts,” said Christopher McDermott, vice president and property product manager, U.S. loss adjusting, Crawford & Company.

“Just as important, if brokers and underwriters identify insureds that have either not increased their limits in the last five years or have shown automatic inflation increases of less than 4% annually, they should contact them to discuss the issue.”

James Finucane, senior economist at Swiss Re, said that “to communicate the potential impact of replacement costs on insurance costs to clients, they can provide transparency about costing elements, trends and forecasts. Proactive outreach could also include economic scenarios to ensure that clients are aware of and prepared for unforeseen economic shifts.”

Jill Dalton, managing director of Aon’s U.S. property risk consulting group, added, “It’s about brokers and insurers consistently communicating with insureds what is happening in the market, the latest renewal trends and what to expect in terms of rates.”

Risk engineers can work with insureds to identify and minimize risks to try to prevent damage and accidents from happening in the first place.

They can achieve this by providing worker safety training, as well as by helping to put in place flood defense systems and supplying safety equipment and technology such as wearables and telematics.

The added benefit for the insured is that if they can prove they have implemented these measures, they can negotiate a better premium. It can also help to speed up the claims process, as they will be able to show what steps they took to protect themselves and their assets.

Accurate Assessment

James Finucane, senior economist, Swiss Re

As replacement costs have shot up due to inflation, it’s paramount that insureds provide their insurer with the actual cost to replace the property or equipment, rather than the book value. They need to get regular appraisals of the replacement value of their asset to ensure that it’s correct.

“There is a big discrepancy between book value, which is what the company said it cost to acquire the equipment or property, and the full replacement value,” said Tracey Ant, The Hartford’s head of middle and large commercial. “Underinsured business owners are likely putting their companies at financial risk.

“When a business doesn’t have an adequate amount of property insurance, the business owner may be responsible for paying the remaining replacement costs when their insurance doesn’t cover the entire claim. These costs can be devastating for a business.”

Insureds must also review their policies to make sure that they have the right coverage and limits in place to ensure they’re protected in the event of a loss. This includes options for inflation indexation and extended replacement cost coverage.

“First and foremost, insureds need to have a thorough understanding of their coverage and what it provides them with from a replacement cost perspective,” said Mike Rouse, U.S. property practice leader at Marsh. “That requires knowing how much risk they are willing to retain and how much they want to transfer.”

Ant added: “To help mitigate the risks of macroeconomic factors, business owners need to be sure they are purchasing adequate insurance to stay ahead of any exposures they might face. Accurate property valuations are an essential component of any property insurance program, yet companies often unknowingly underreport the value of their property assets, potentially leaving them underinsured.

“To support accurate valuation, it’s critical for a business owner to provide information about their property that’s as complete and in-depth as possible. This includes the size, age and use of the property, as well as any specific or unique construction details.”

Other measures should include building emergency funds, budgeting for increased costs and investing in risk mitigation technologies. Insureds can also use self-insurance to manage their insurability and insurance costs.

In addition, when buying property coverage, owners need to consider the insurance-to-value ratio — the ratio of a property’s insured value relative to the cost of replacing that building. The more information and detail an insurer has about the makeup of a property, the more accurate their valuation assessment and premiums will be.

“At the end of the day, insureds need to be able to tell their own story about their replacement costs and how they arrived at those values without being told by the insurance company what it thinks they should be,” Dalton said.

“They also need to be confident and comfortable with the values they are reporting so that they can avoid any margin clauses or coinsurance.” &