Captives

Corporations Get Creative With Cells

Cell captives have become extremely popular self-insurance tools for companies of various sizes across all sectors, with cell legislation enacted in more than half of U.S. states and cell formations now outstripping stand-alone captive formations in many onshore and offshore captive domiciles.

Protected cell companies (PCCs, also known as a segregated accounts companies or segregated portfolio companies) consist of a core company that writes and administers ring-fenced insurance policies in underlying cells, whose policies and accounts are segregated from other cells in the PCC.

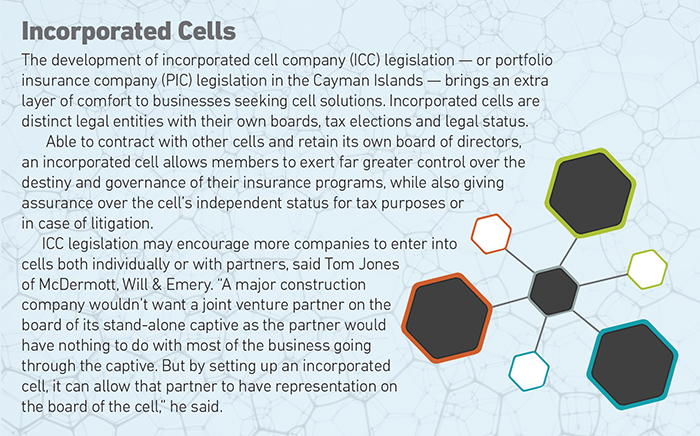

The recent development of incorporated cell company (ICC) legislation in a handful of jurisdictions enhances PCC features by granting each cell distinct legal status.

As well as being quick to set up, cells require significantly less capitalization than stand-alone captives, while shared costs among the participants and core lead to economies of scale. It is little surprise that since the first PCC was formed in Guernsey in 1997, they have proliferated and broadened.

“Risks written through cells are becoming more sophisticated, expanding beyond traditional medical malpractice, workers’ compensation and property insurance,” said Paul Scrivener, a partner in the Cayman Islands’ law firm Solomon Harris.

Cells are being touted, for example, as a potential solution to cyber risk, one of the insurance industry’s great challenges.

Cells for Every Risk

“If you have a structure with different risk profiles within different cells, it may make sense to put cyber risk in a separate cell rather than co-mingle it with traditional lines of insurance as it is very different and unique,” said Scrivener.

Paul Scrivener, partner, Solomon Harris

“Some have suggested using a cyber cell because you are looking at low frequency, high severity situations,” added Tom Jones, partner with McDermott, Will and Emery. Questions remain, however, over how best to address coverage terms, exclusions and payout limits, he said.

Cells are also growing in popularity in the health care space, particularly for medical malpractice risks.

“Hospitals may set up cells for independent physicians or group faculty plans if they want to assist them with insurance but don’t want to co-mingle the loss reserves,” Jones said.

Scrivener recently converted a single parent health care captive to a cell structure so it could put its existing hospital program into one cell and create a second cell to insure the risks of the self-insured physicians within the hospital.

Ascension Insurance Services set up Cayman’s first portfolio insurance company, AARIS, in 2015 to offer workers’ compensation solutions to agribusinesses, but now intends to roll out flexible workers’ comp cells to other sectors including the trucking and automobile racing industries.

“We’re getting calls from all around the country,” said Paul Tamburri, Ascension’s West Coast risk management practice leader, adding that the next step could be to write employee benefits stop loss through AARIS.

Cells can offer a fast route into captive insurance for employee benefits programs, while many regulators have yet to find a comfort level with stand-alone employee benefits captives.

“Getting the whole cell structure approved up-front makes it relatively easy to add cells. Instead of taking six months to get approval, we can get a cell approved in a matter of weeks,” said Karl Huish, president of captive services for Artex Risk Solutions, which runs a PCC-like employee benefits series business unit named Sentinel Indemnity in Delaware.

“Getting the whole cell structure approved up-front makes it relatively easy to add cells. Instead of taking six months to get approval, we can get a cell approved in a matter of weeks.” – Karl Huish, president of captive services, Artex Risk Solutions

“The cells in Sentinel each have different employee benefit captive structures, including one that is for a group of credit unions who want to pool risk together for their health insurance,” he added.

According to Guernsey Finance, multinational corporations can use cells as fronting vehicles through which to gain access to the reinsurance market. A cell can be used to issue an insurance policy to the insured that is mirrored by a policy between the cell and a reinsurer, and while the cell retains no risk, the corporation benefits from access to cheaper wholesale reinsurance cover.

The ability for numerous small companies to group their insurance risks in a cell means the self-insurance business is no longer reserved for big corporations. Huish believes a group of insureds must have projected annual losses in the region of $5 million or above to justify forming a cell, while that figure would be closer to $3.5 million for individual cell owners.

Insured Turns Insurer

More than simply participating in their own risks and enjoying greater control and premium savings from self-insurance, an increasing number of companies see PCCs as an opportunity to generate cash flows while strengthening bonds with business counterparts. Indeed, any company comfortable with the self-insurance concept can set up its own PCC to offer insurance solutions to third-party clients, suppliers or partners.

Not only does the sponsor of the PCC get closer to the risk of companies that affect its own risk profile, but it can also add value to its service propositions by offering valued third parties a quick, cheap route into self-insurance.

“Setting up your own PCC is a way of locking in clients, strengthening relationships and generating revenues, while also offering profit sharing opportunities between the PCC owner and its clients,” said Clive James, consultant at Artex Risk Solutions.

“Setting up your own PCC is a way of locking in clients, strengthening relationships and generating revenues, while also offering profit sharing opportunities between the PCC owner and its clients,” said Clive James, consultant at Artex Risk Solutions.

While this may be a natural fit for financial services firms, the concept can be applied to any sector, and may be particularly useful for those that operate on a project-by-project basis.

Construction firms, for example, are setting up PCCs through which the underlying cells write segregated insurance coverage for distinct projects, partners or groups of subcontractors. Freight storage unit owners are already using cells to self-insure the fire, theft and flood insurance they provide to licensees of the units, and there are myriad opportunities for health care organizations to offer insurance across their networks via cells.

Companies that lack the insurance expertise to run a PCC themselves would outsource this responsibility to an insurance manager in the same way stand-alone captive administration is outsourced — at a similar cost.

As PCC sponsors must ultimately compete with guaranteed cost options in the commercial marketplace, Tamburri noted it is essential to educate potential clients that participation is both a long term commitment and also an opportunity to recoup underwriting profits they would otherwise lose if they stayed with commercial insurers.

“One hurdle is getting data from prospective clients,” said Tamburri. “It’s a lot of work for them to get together historical loss and exposure information. Smaller companies may wish to join the group but fear that they will do a lot of work only for the cell not to get off the ground.”

Such is the decision all companies must make when considering self-insurance, whether taking an individual cell or going a step further by forming a full PCC for third parties to join. What is clear is that cells give risk managers more options than ever before. And when insured becomes insurer, it is surely a sign of insurance industry evolution and innovation.