Reputational Risk

Claims and Culture

For the past year, Fox News appeared to spend as much time making news as it did reporting it. Lurid accounts of sexual harassment involving the late CEO Roger Ailes and on-air host Bill O’Reilly alienated advertisers, stained the network’s reputation, and continue to cost 21st Century Fox millions on a quarterly basis.

Additional firings and suspensions this summer of top personnel — also for sexual harassment — suggest that Fox’s problems are not yet in the rear view mirror.

In February, Uber stole some of the spotlight from Fox after a female former employee published a startling blog post laying bare the company’s “bro culture” where sexual harassment and discrimination were allowed to flourish.

Uber has since fired more than 20 employees, some of them senior executives, and 40 additional employees were reprimanded or referred to counseling and training. CEO Travis Kalanick was forced to step down in June.

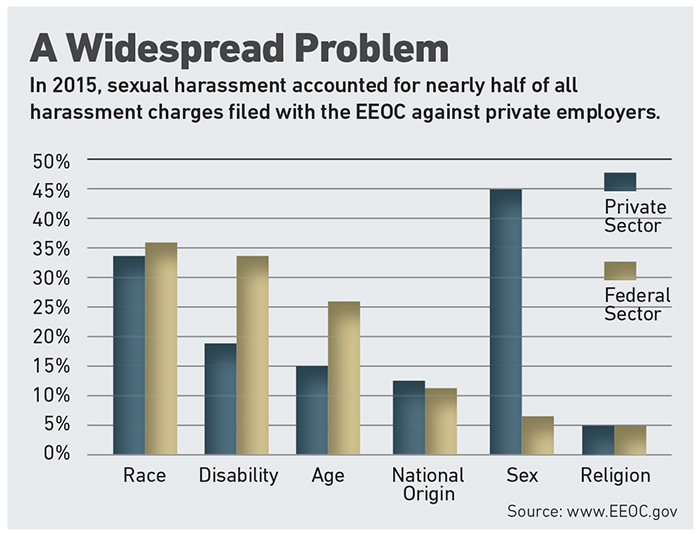

The highly public nature of Uber’s and Fox’s woes is atypical. Approximately 15,000 sexual harassment cases are brought to the Equal Employment Opportunity Commission (EEOC) each year. Those found to be viable are often settled quietly, but at no small expense to the company, said Chris Williams, employment practices liability product manager for Travelers.

Susan Strauss, principal, Strauss Consulting

Cases that reach a jury pose a new level of risk. Public disclosure of emails, voicemails or other communications can be “tremendously embarrassing” for the company, said Williams, and there is also a trend toward juries wanting to punish companies that are aware of sexual harassment issues but failed to take any action.

“Whether it goes to court or not it still impacts their bottom line,” said consultant and trainer Susan Strauss, an expert in workplace harassment and bullying. “Morale drops, productivity drops and absenteeism increases. Employees tend to suffer from an increase in the amount of physical ailments — everything from colds to GI problems to heart attacks and migraine headaches.”

There can be severe psychological ramifications for the victims, she added, including depression and suicidal feelings. Some victims might need to take FMLA leave, or might require accommodation under the ADA.

All of which impacts the culture and productivity of the organization, she said. “If word gets out … then they’ve got a poor reputation out in the community and within their industry. It’s just bad all over. Then the employees wonder why isn’t management doing something about it. There’s a loss of trust.”

The potential for this level of damage, said Williams, should serve as incentive to put risk management strategies and techniques in place.

Many Remain Uncovered

Employment practices liability insurance can help defray the cost of legal defense as well as costs related to judgments or settlements, making it an ideal solution for any company that would be hard-pressed to pay such costs out of pocket. Yet take-up on EPLI remains moderate.

Gross written premium for EPLI in 2015 was $2.1 billion, according to MarketStance, despite a 2003 Best’s Review prediction that the EPLI market would grow to around $7 billion “in the next few years.”

“Insurers, generally speaking, choose very good lawyers to defend cases. But oftentimes in these high stakes situations, they aren’t the firm that the client wants.” — Bill Boeck, senior vice president, Insurance and Claims Counsel for Lockton

Growth of the segment has slowed, partially due to some of the available premium shifting into bundled management liability policies that include EPLI as well as D&O and other coverages. A main point of concern is that 60 percent of non-buyers mistakenly assume their EPL risks are protected under other policies, according to Gen Re.

Larger employers, and those with the most insurance savvy, are significantly more likely to transfer their EPL risks than smaller employers, even though small to mid-sized employers stand to suffer more in the face of a hefty judgement or settlement.

“If you think about the cost of one settlement or even trying one of these cases, it’s not uncommon for the legal fees to go up to $250,000 or more,” said Williams.

“And then if you lose, you’re also responsible for the plaintiff attorney’s fees. So I think a key risk management strategy really does have to be an employment practices liability policy.”

EPLI premiums are based on a variety of factors, including company size, industry, and location. But underwriters also want to know what the company’s policy on sexual harassment is, and what procedures are in place to enforce that policy. A robust reporting process is vital, as well as a swift and transparent investigation procedure that ensures a resolution.

Some situations can be resolved by coaching the harasser, but some situations require that the harasser be terminated because the conduct is simply unacceptable, said Williams.

“What an underwriter needs to see if it’s a good risk, is the culture of the company, the weight given to their employment policies and procedures, and how seriously they take the investigation and reporting of any sort of incidents or claims,” said Edward McNally, Chief Underwriting Officer, Lockton Affinity.

Edward McNally, Chief Underwriting Officer, Lockton Affinity

Underwriters may apply other tools, including data from EEOC reporting forms. Employee comments on sites like glassdoor.com can also provide insight into how the company operates behind closed doors.

“It’s really hard, as an underwriting organization to get at the corporate culture through just a paper application,” said Williams.

One issue risk managers may want to raise while negotiating an EPLI policy is the selection of counsel, said Bill Boeck, senior vice president, Insurance and Claims Counsel for Lockton.

In a high stakes EPL event, he said, “many clients are very concerned about having exactly the right lawyer defending the claim.” But EPL policies often give the insurer the ability to select defense counsel.

“Insurers, generally speaking, choose very good lawyers to defend cases. But oftentimes in these high stakes situations, they aren’t the firm that the client wants.”

Don’t wait until a claim occurs to raise the issue, Boeck cautioned. Once the policy has been triggered, “the insurer will enforce whatever right it has.”

Additional Coverage

In an age of social media hyperfocus and boycott campaigns run by hashtag, risk managers should certainly be thinking about how a sexual harassment claim could impact their organization.

“You’re not only worried about the claim itself you’re worried about what it’s going to do to your business. Is it going to lead people to stop doing business with the company?” said Boeck. “People decide ‘I don’t like what Uber’s doing so I’m going to use Lyft.’ All of a sudden Uber’s business falls off.

Is there something a good company can do to recover from that? The answer is yes — there may be possible solutions,” he said, referring specifically to reputational risk coverage.

“If I feel like my senior executives or my board are really worried about reputational damage that flows from something like this, then that’s something I would want to explore.”

The coverage can be expensive, and laborious to underwrite, Boeck said. But for some companies, it may make good financial sense.

“A good policy is always going to be a bespoke policy,” he said. “It’s going to be custom designed for a particular client.

Training and Measuring

Experts unanimously agreed that training is the best preventive strategy to minimize the risk of claims as well as improve an organization’s risk profile. But companies that try to get by doing the bare minimum won’t be doing themselves any favors, said Strauss.

Too many companies, she said, expect HR to handle training internally, even if the staff aren’t trained in the subject. Worse, some rely on one-size-fits-all online training that has no effect.

“You have to do more than online training — that really doesn’t work … it’s the same old boring stuff and it might only focus on the legalese and not the practicality. It’s got to be good training, by somebody that knows what they’re doing.”

Strauss recommends a half-day training session for employees and a full day for management. Managers need guidance on what ethical and legal responsibilities are, she said. And “they need to be trained in how to intervene. They need to be able to recognize some of the more subtle, nuanced forms of harassment and know how to confront it when they see it.”

Carrie Kurzon, National EPLI Product Manager at The Hartford, concurred that insurers are paying attention to clients’ training initiatives.

“Companies that conduct management-level training to ensure that internal complaints are processed appropriately and in compliance with articulated policies would tend to be more favorable accounts for insurers,” she said.

“Training is not just once, added Strauss. “It’s got to be ongoing. And you don’t do the same training year after year, you add different aspects to it.”

But Strauss stressed that training is only one piece of the pie, especially for any company with an unfavorable EPL loss history.

“The big first step is to recognize that the problem exists and then to define it,” said Strauss. “They have to be open to acknowledging the culture and that’s a hard thing to do in and of itself.”

Strauss suggests creating a task force comprised of people across the organization — from maintenance engineers all the way up to the corner office. The task force can conduct a baseline survey including interviews, in order to assess the scope of the problems and the obstacles to eliminating those problems.

Lockton Affinity’s McNally added that a thorough audit of company data can be an essential tool to identify those problems.

“A lot of companies don’t engage in this behavior of statistical analysis within the HR practices. You do a lot of auditing of everything else within your business, but HR’s kind of left out of that loop.”

“While it is impossible to prevent a sexual harassment claim from being filed, by focusing on preparation and protection, risk managers can reduce the likelihood of such a claim and mitigate long-term impacts such as costly litigation.” — Carrie Kurzon, National EPLI Product Manager, The Hartford

Assessing the company’s employment claims and litigation statistics as compared to national data is one way to spot patterns and anomalies, suggested McNally. It can be telling if claims coming from any particular class of people are out of proportion with the larger picture of where claims are coming from.

“You’re boiling a very human condition down to the math,” said McNally. But it will help to isolate trends that need to be unpacked and understood.

“That high level of statistical awareness of the claims that you’re getting and the settlement rates, against the general market, would be a huge benefit to risk managers,” he said. “And I think it would also drive that conversation that’s lacking for a lot of companies — where the human resource department and the legal department and the risk management department aren’t necessarily wholly tied into each other [with regard to] employment litigation.”

Armed with that knowledge, “establish a strategic plan,” said Strauss. That plan should include goals and measurable objectives that can be monitored, especially throughout the first year.

Travelers’ Williams said that a couple of decades ago, he would have predicted that by now, corporate America would’ve figured out how not to have these claims. “I’ve done a 180 on that; and I don’t think we’ll ever eradicate them.” That’s because there’s never going to be a way to control every interaction between employees on the shop or office floor, he said.

“While it is impossible to prevent a sexual harassment claim from being filed,” said Kurzon, “by focusing on preparation and protection, risk managers can reduce the likelihood of such a claim and mitigate long-term impacts such as costly litigation.”&