Solar Power Risks

The Perils of Being Green

Fighting an 11-alarm conflagration at the Delanco, N.J., Dietz & Watson warehouse this past Labor Day weekend, firefighters were sandwiched between a rock and a hard place — between the duty to protect their community and concern for their own safety. They satisfied both by containing the fire and preventing it from spreading. What was lost, however, was the meat and cheese manufacturer’s five-story, 300,000-square-foot cold-storage facility. That, and the peace of mind of risk managers with solar panels on their buildings’ roofs.

“Baloney!” you say? “What’s the big deal? That doesn’t sound any different than any other warehouse fire.”

According to news reports, the fire took dozens of firefighters more than 24 hours to get it under control. Due to the massive plumes of smoke, locals were told to remain indoors. The fire smoldered for days afterward. And for days, even weeks after, most residents chose to remain indoors — or fled the neighborhood — because of the smell of rotting meat. An estimated 8 million pounds of cold cuts had been stored in the facility.

“Anyone who lives or works near there will tell you it stinks. We know that it does, and that it has impacted their quality of life,” wrote D&W CEO Louis J. Eni Jr. on the company website, in a letter to concerned customers and neighbors. (Dietz & Watson declined comment for this article.)

In his digital note, Eni admitted that the reason it took so long for cleanup crews to begin hauling meat from the plant, beside the fire flareups, was the risk of shock from the thousands of potentially still-energized solar panels that had been on the building’s roof.

Those very same thousands of solar panels had obstructed firefighters’ efforts in the first place. (A water shortage was purportedly also to blame.)

This national news event caught the attention of corporate risk managers, property developers and their insurers, several of whom agreed to speak with Risk & Insurance® about their approach to solar panels — from a loss control and underwriting point of view.

The Enemy?

A Reuters news article about the Delanco fire referred to solar panels as the “enemy” of firefighters, who feared electrical shock from contacting the panels. As the D&W fire illustrated, anything that causes that kind of trepidation on the part of firefighters hampers fire-control efforts.

Joe McGinnis, a consultant with ESIS Health Safety & Environmental, explained that rooftop access is important, particularly during commercial fires, because of the need to do “vertical ventilation.” This involves firefighters climbing onto the roof and cutting holes in it — in many cases directly above the fire — which allows heat, smoke and toxic gases to escape. Firefighters can then enter the inside of the building and better attack the fire. Without the ability to do vertical ventilation, continued McGinnis, firefighters most likely will carry out defensive measures, meaning they will fight the fire strictly from the outside. That increases the risk of a total loss.

“Do I think we’d have had a different outcome if we could get on the roof? Sure,” Delanco Deputy Fire Chief Robert Hubler said to news reporters following the Dietz & Watson incident.

The frustration comes through in Hubler’s words, but it is not entirely fair to blame solar panels. A spokesman for the Solar Energy Industries Association, Ken Johnson, put some of the onus on the firefighters themselves.

“Firefighters don’t have a good idea of how solar works. It’s incumbent on us to do a better job in educating them,” the spokesman told Reuters.

That may sound defensive, coming from the lobbying group for manufacturers after a massive loss related to their product, but the view is echoed by experts.

Ed Donaghy, director of property management for Pennsylvania-based Hankin Group, reported that his employer, a builder and developer with 1.5 million square feet of commercial space in 25 buildings, including the green XL Group office in Exton, Pa., has been placing solar panels on roofs since 2010. Initially, they installed them like “another piece of equipment.” But then he started to learn more about their safety and loss-control issues. Then came the D&W fire and another local event, a fire at Owen J. Roberts High School in Pottstown, Pa., again involving solar panels impeding firefighters’ efforts.

The issue clarified in Donaghy’s mind. Many firefighters are unsure what to do with solar panels, he said.

“Nobody knows what to do in that case,” Donaghy said. “It’s more of a fear factor.”

Steve Bushnell, director of product development in commercial insurance at Fireman’s Fund, was concerned when he read the news reports from Dietz & Watson fire about firemen not knowing how to access roofs with solar panels.

“Raising the education of firefighters is something that is critical,” Bushnell said.

It’s not so much that firemen can’t figure out how to handle these types of incidents; they have, but the knowledge has not been distributed, digested or standardized. Fireman’s Fund developed underwriting and loss-control positions for rooftop solar in 2010, but they were beat by the California Department of Forestry and Fire Protection (CAL FIRE). CAL FIRE released a solar photovoltaic guideline in April 2008, in partnership with the solar industry, about installing panels on commercial and residential properties.

Underwriter Awareness

Underwriters, it appears, have been aware of how solar panels change a building’s risk dynamic on several levels, said Jeff Beauman, vice president and manager, all risk underwriting, at FM Global. Underwriters have considered how well a roof can withstand the added weight of solar panels, doing much the same structural calculations as they would for any rooftop equipment. They have factored in if panel installations could compromise the water seal of a roof, or if panels could act like sails during windstorms.

Bushnell noted that the Fireman’s Fund’s 2010 guidelines address hail damage to panels as well as theft.

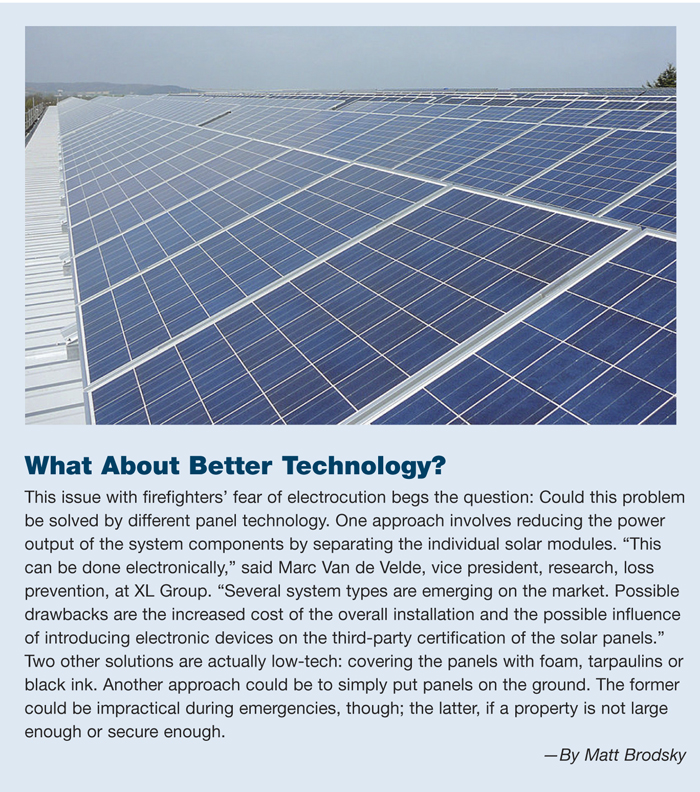

As far back as 2010, XL Group has been examining solar panels and loss prevention related to fire, said Marc Van de Velde, vice president, research, loss prevention, at XL Group.

As far back as 2010, XL Group has been examining solar panels and loss prevention related to fire, said Marc Van de Velde, vice president, research, loss prevention, at XL Group.

“A photovoltaic installation on a rooftop introduces a large number of electrical components in an area where there are normally few present. This increases the probability of a roof fire significantly,” Van de Velde said.

And as for the issue of solar panels contributing to fire losses by inhibiting firefighter activity, Beauman is aware of discussions in the industry about that as well.

“These news articles have caught people’s attention,” he added.

With awareness spreading, underwriters may now respond differently to properties with rooftop panels. For instance, said Beauman, an underwriter could consider a complete loss more probable and adjust premiums accordingly.

Help for Solar Owners

Are risk managers adjusting their perspectives about rooftop panels, much in the same way that Hankin Group’s Donaghy has?

Beauman said that most of the insureds of his Johnston, R.I.-based property mutual are represented by savvy risk managers. But as for risk managers in general, he conceded that news articles about Dietz & Watson and other fires may be the first time that some risk managers are learning of this issue.

Yet it’s never too late to learn. And one doesn’t need a CAL FIRE guidebook (PDF) to get started (though it is available for free online). Photovoltaic self-help includes practical design, engineering and risk management steps.

Take Bushnell’s big tip: communication with the local fire department. Indeed, big commercial firms should already have a relationship with their fire departments, panels or not. Companies can also be conducting dry-run fire drills. With rooftop panels in mind, that can be a time for firefighters and property owners to discuss how to shut down a system, how best to access the roof and where to locate inverter boxes.

XL’s Van de Velde recommended involving all stakeholders — installers, owners, insurers and firefighters — at the outset during the planning phase of an installation.

“At this point, possible intervention tactics can be discussed and the actual installation layout adapted to create large enough access areas that can be used by the fire department in case of emergency,” he said.

The key here, as CAL FIRE explained in its guidelines, is to not wallpaper a roof with panels. At the very least, leave paths on the roof among the panels. Added McGinnis of ESIS HSE, one can refine this technique by knowing where the building’s fire hazard spots are — where fires could most likely occur — and purposefully leaving the rooftop bare above them.

Another step could be to insert roof access points, such as skylights and hatches, which could facilitate firefighters’ ability to perform vertical ventilation of the roof without cutting holes.

Or you could “engineer out … the entire risk of people going to the roof altogether” through a mechanical ventilation system. All of this can be designed at the outset of construction or installation of panels — or as retrofits after the fact.

Then again, there is another option. Property owners and underwriters could shy away from panels altogether until firefighters begin to follow the lead of California, or devise their own consistent policies for handling rooftop solar panels.

As for Hankin Group, it initially installed solar panels to take advantage of the lucrative ESREX market, where producers of green energy sell it to energy utilities. That market is currently oversaturated with supply in Pennsylvania, with ESREX prices dropping from $300 levels to around $17, according to Donaghy. So at least in the Keystone State, the firm is opting not to install solar panels because the economics currently don’t make sense — not because of the risks.

Yet when the economics do make sense again, perhaps insurance and loss-control issues will factor into the calculations. Or not.

“A lot of times people think of the roof as free money,” said Beauman. “Why not put it into productive use?”

The roof, though, is there for other reasons — “so you can run your business.”

If somebody could get Dietz & Watson to talk turkey about the costs of their warehouse fire, there’s a good chance they might agree.