A New Solution to Address Construction’s Growing Weather Problem

The U.S. construction industry has been enjoying steady growth since pulling out of the depths of the recession. Since then, spending on both public and private projects combined has risen from $788 billion in 2011 to $1.23 trillion in 2017, a 156 percent increase.

But a concurrent trend is threatening continued growth — global warming and increasingly volatile weather.

“Construction activities are directly affected by weather events. No one’s pouring concrete in the rain or in extreme temperatures, because it affects the durability of the product in the end,” said Mike DeLio, an analyst and construction industry expert with Aon.

Bad weather causes project delays in a number of ways — creating unsafe conditions to do work, physically damaging materials or equipment, blocking access to a job site or causing supply chain disruptions. Unforeseen delays can force the contractor to eat the loss of compensation or incur contract penalties. The dollars quickly pile up.

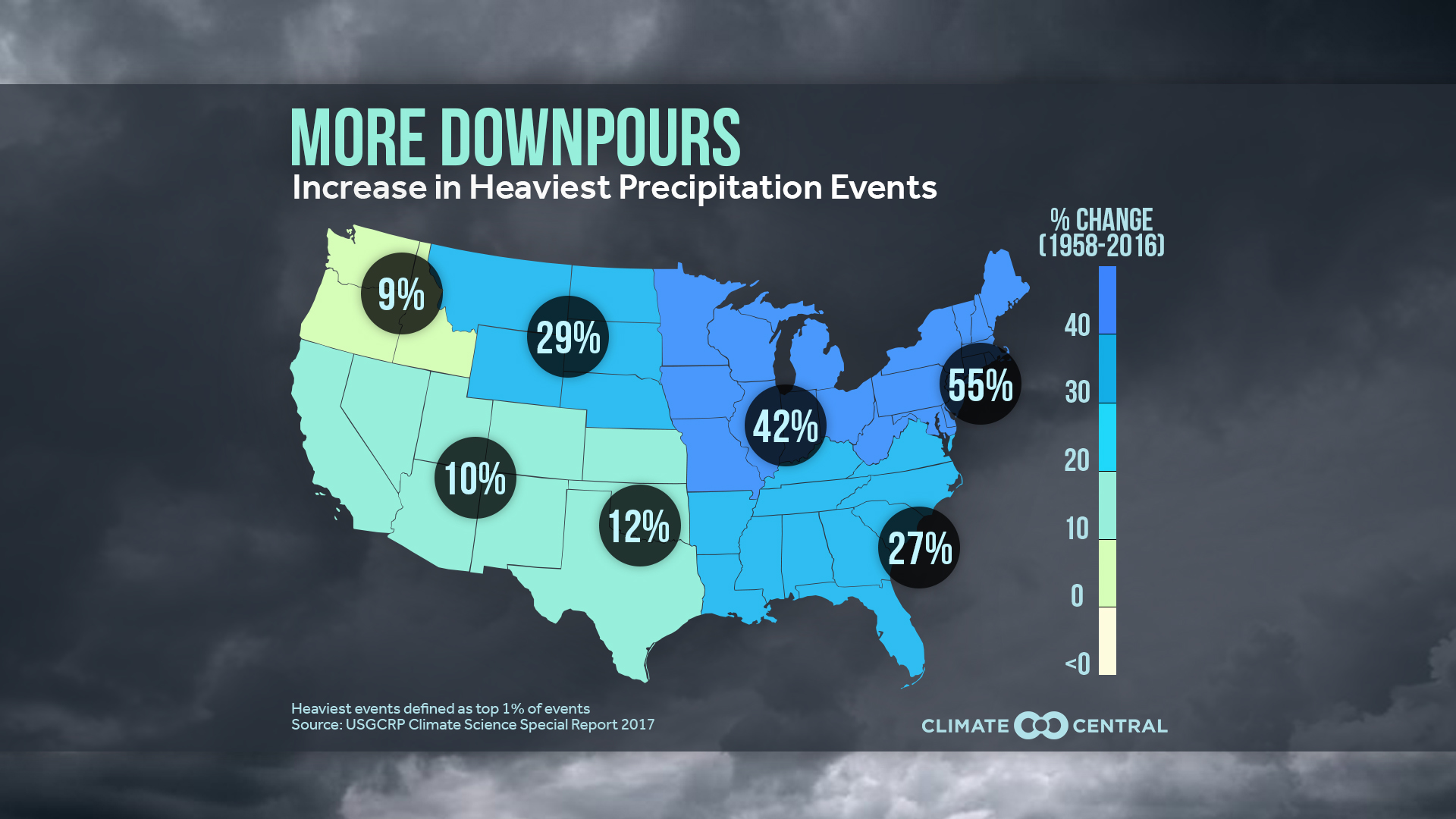

Over the previous 50 years, Southwestern states have seen at least a 10 percent increase in heavy downpours — defined as rainfall that exceeds the average for that region — while states in the Northeast have seen a 55 percent increase.

“This past year, a pipeline contractor was digging miles and miles of trench. A significant storm came through and left 10 inches of rain over seven days and flooded in all of their work. They had to start over, and it equated to a $25 million loss,” DeLio said.

According to Climate Central, “For every 1°F of warming, the saturation level of the atmosphere increases by about 4 percent. This means more water is available to condense into precipitation, and it can come down in heavier downpours.” According to NASA’s Goddard Institute for Space Studies, “the average global temperature on Earth has increased by about 1.4° Fahrenheit since 1880.” Heavier and more frequent downpours have indeed accompanied the warm up. Over the previous 50 years, Southwestern states have seen at least a 10 percent increase in heavy downpours — defined as rainfall that exceeds the average for that region — while states in the Northeast have seen a 55 percent increase.

Source: USGCRP Climate Science Special Report 2017

While weather risk itself is nothing new, the increasing intensity, frequency and unpredictability of weather events — driven by global warming — are challenging traditional methods contractors use to account for the exposure in project planning and contract negotiating.

A study looking at the impact of weather events on construction projects in the UK found that weather extends project duration by an average of 21 percent. However, when contractors referenced climate data in the planning process, project duration reduced by 16 percent.

That would seem like a common-sense conclusion, but in fact many contractors do not draw from reliable data sources when factoring weather contingencies into project contracts.

“We’re finding that there are very few contractors who are sophisticated in how they’re looking at this risk and actually pulling in satellite imagery data to understand their exposure. More often than not, they basically pull a number out of a hat based on their past experiences,” DeLio said.

The effects of climate change mean those past experiences are no longer reliable indicators of the future.

“There’s increased volatility in rainfall, in hot and cold days, and high winds. It’s not as predictable. In the past 5 or 6 years, our contractor clients have identified in their annual reports that weather is a major risk to their financial performance,” DeLio said.

A New Solution to Contend with Unpredictability

Contractors essentially have two options to better manage weather risk. The first is to get better at quantifying their exposure at a more granular level. Gaining a more accurate picture of the risk enables them to more effectively negotiate realistic contingencies into their contracts with project owners. That means gathering more weather data and analyzing past projects to correlate specific weather conditions with specific impacts as far as lost time or physical damage.

“We have access to satellite data. We’ll help them identify and quantify that risk and see if there is potential for serious delays in the project,” DeLio said. “It starts with identifying their exposures, whether it’s rainfall, or extreme heat. And then we determine what that means at certain thresholds. For example, if it rains one inch, we lose one day of work. If it’s above 90 degrees, workers take more breaks, which ultimately add up to another lost day. Once you have that degree of specificity, you can either negotiate that into the contract or look at third party risk transfer solutions.”

“We’re finding that there are very few contractors who are sophisticated in how they’re looking at this risk and actually pulling in satellite imagery data to understand their exposure. More often than not, they basically pull a number out of a hat based on their past experiences.”— Mike DeLio, analyst, Aon

Those risk transfer solutions, in the form of parametric coverage, are a recent development. What distinguishes a parametric policy from other standard coverages like general liability is that parametric polices are triggered by events, not by losses.

If an owner won’t accept more risk in their contract, and the contractor can’t afford to take on the risk themselves, the contractor can take those same thresholds determined through data analysis to build a parametric coverage specific to that project. For example, wind speeds exceeding 15 mph may be established as a level which would halt crane work, and therefore would be set as a policy trigger. If wind exceeds that speed for a certain amount of time as the trigger dictates, the policy will pay out a predetermined amount regardless of any damages incurred.

“Its effect is similar to a non-damage business interruption policy,” DeLio said.

Because they are designed to cover outlier events, parametric policies can help fill in coverage gaps when combined with other standard policies. “Combinations of standard coverage with parametric coverages can be very effective in helping contractors cover their bases as severe weather gets more intense and more unpredictable,” DeLio said. With new bids in 2019 on track to match 2018 at a value of $808 billion, finding ways to manage Mother Nature will be critical to contractors’ success. &