Insurance Agency M&A Activity Slows as Private Equity Tightens Grip on Market

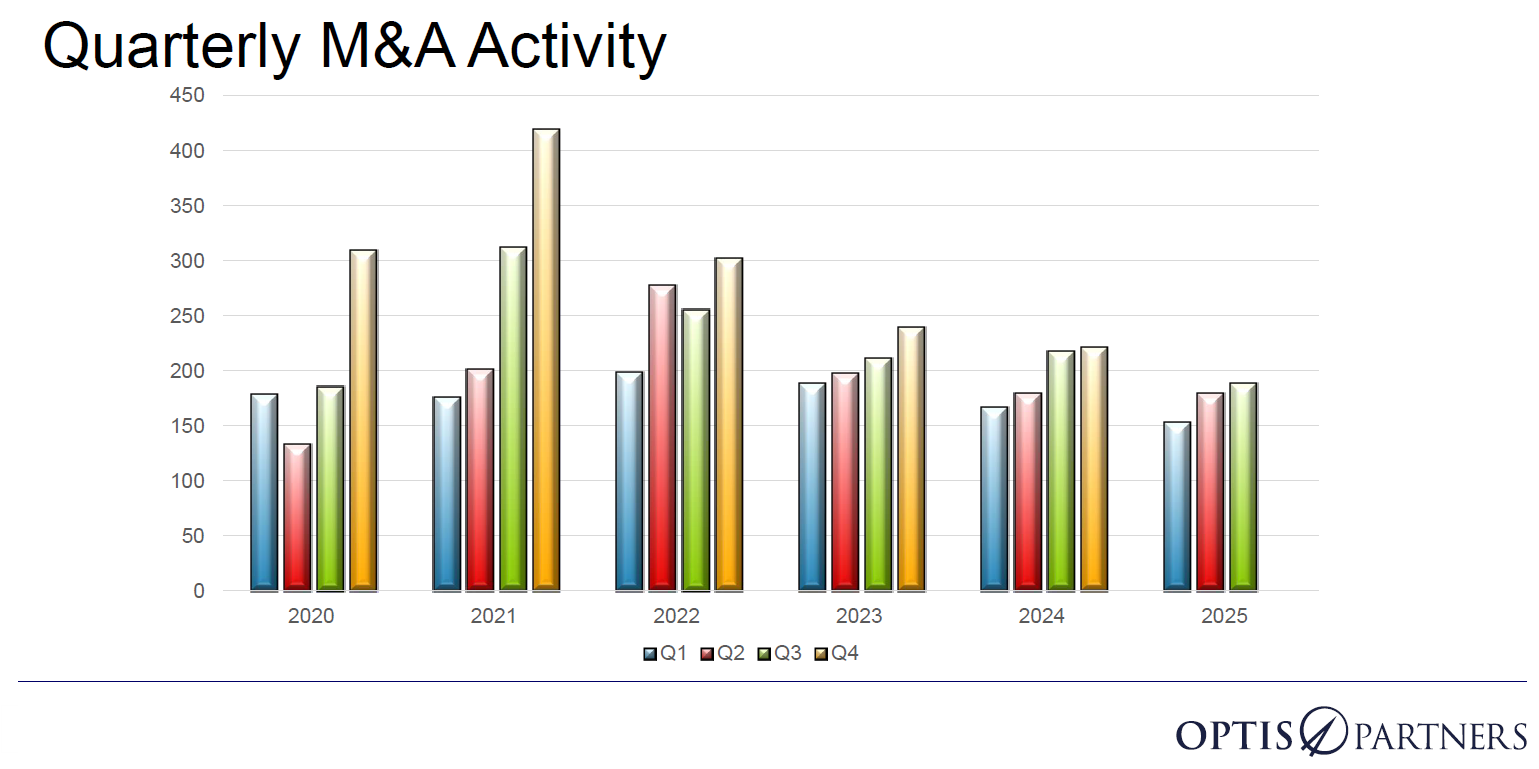

The insurance agency merger and acquisition market recorded 520 transactions through the first three quarters of 2025, marking a 7% decline from the same period last year, according to OPTIS Partners’ Q3 2025 Agent & Broker Merger & Acquisition Update.

The third quarter of 2025 saw 188 announced transactions. Although this was up from 179 deals in Q2, it represented a 13% year-over-year decrease and falls 20% below the previous five-year average, the report said. This deceleration reflects a broader trend, with the trailing 12-month deal count of 741 transactions hitting its lowest point since Q3 2020, when 647 deals were recorded.

Market concentration has intensified significantly, according to OPTIS Partners. The number of unique buyers has narrowed to just 96 in the current period from 152 in September 2021, while the top 10% of buyers now control 56% of all deals completed, up from 46% four years ago.

BroadStreet Partners maintained its position as the most active acquirer with 57 transactions year-to-date, though this represented a 21% decline from its 2024 pace. Hub International followed with 38 deals, down 12% from the prior year and 11% below its five-year average.

Among buyers completing at least 20 transactions, some firms significantly accelerated their acquisition pace, the report said. Alera Group doubled its activity with a 100% increase, while HighStreet Partners and King Risk Partners posted gains of 75% and 53%, respectively.

Private Equity Dominance Creates New Market Dynamics

The shift in buyer composition has reshaped the competitive landscape for independent agencies. Private equity-backed and hybrid firms completed between 68% and 76% of all transactions over the past four years, while privately-owned buyers saw their share decline to 15% from 23% of deals during the same period. The number of privately-owned buyers has dropped dramatically to 42 currently from 85 in 2021, the report said.

Publicly traded brokers maintained a relatively stable but minor presence, accounting for 5% to 9% of total transactions. This buyer type composition has remained “relatively consistent” across trailing four-quarter periods since September 2021, suggesting the current market structure may represent a new normal.

The consolidation trend extended to major transactions, with Arthur J. Gallagher announcing its acquisition of AssuredPartners for $2.9 billion and Brown & Brown purchasing Accession Risk Management for $1.7 billion, both completed in August 2025.

Market Outlook Points to Continued Moderation

Looking ahead to the fourth quarter of 2025, OPTIS Partners expects activity to remain “equal to or slightly below” Q4 2024 levels, continuing the downward trend that began with a 28% drop in Q4 2022. This projection suggests the market has settled into a more moderate pace of consolidation.

View the full report here. &