Container Shipping

A Sea Change in Risk

It all seemed to happen in a heartbeat: A struggling industry went from bad to worse as one of its largest members filed for bankruptcy. Panic set in among Hanjin Shipping Co.’s customers over goods stranded at sea and litigation lawyers began lining global ports to pick up the pieces.

Suddenly, the risks posed to container shipping by overcapacity, low profitability, and volatile or inadequate pricing crystalized. What, asked other ocean shippers, did this mean for us?

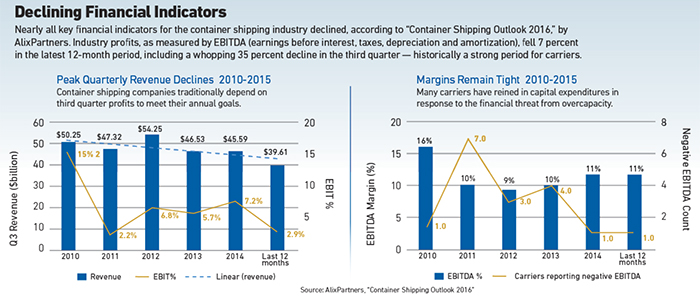

Jim Blaeser pulled no punches when answering that question. In a study in February of last year, his New York employer AlixPartners warned that piecemeal cost-cutting, vessel-idling or slow-steaming in maritime container shipping would do little to curb overcapacity and stem falling profitability and precarious cash flow.

Jim Blaeser, vice president, AlixPartners

In fact, said the company VP, things would likely only get worse unless industry embraced a major alternative: consolidation.

Was AlixPartners’ prediction borne out? Well partly, said Blaeser. “The first three quarters were dismal as we called out; the fourth quarter when results are published in full by the companies should be considerably better. But I think the jury is out on whether carriers will be able to ride that wave into 2017.”

Blaeser said the idea that higher rates sustained into the Chinese New Year will chase the industry’s blues away were “wishful thinking.”

At the same time, Blaeser said, consolidation will place more and different demands on risk managers.

As fewer operators like Maersk and MSC control more capacity, “you’ll need to have a much stronger global reach for corporate control and command to ensure that your risks are understood and that they’re appropriately mitigated.”

By definition, the focus as a risk manager shifts “from your own backyard to a global field of play,” he said.

Consolidate, Communicate … Convert?

Where that field of play looms particularly large is information.

“Ocean freight information is just terrible across the board,” said Blaeser. That stems in part from merger integration of companies with “three, four, five systems handling different pieces of information,” such as for truck, terminal and vessel operations.

“I would argue that, as consolidation takes root and there are fewer carriers, inherently information has to get better,” Blaeser said. That may happen as rates improve and companies spend more on effective software information management tools.

Rick Roberts, director of risk management at Connecticut’s Ensign-Bickford Industries (EBI), is sufficiently alarmed by this and other news to have begun reviewing his policies and risk management strategies.

But it’s not just the risk posed by overcapacity, it’s the risk of consolidation itself.

EBI transports hazardous military goods to Europe and pet food to South America. Insufficient information and possible changes in global routes as companies merge their respective customer bases, for example, give him pause.

“I see we’re going to have some issues where routes are changing and how long it could take for our products to get places. Maybe it used to take 10 days to two weeks and now maybe it takes a month.”

For his part, Ali Rizvi, senior vice president at Marsh in Houston, said the three biggest challenges shippers face are fuel, crew and ship management. Consolidation obviously allows merged companies to use crew more efficiently and renegotiate bunker fuels, while economies of scale present opportunities for more efficient operations overall.

Ali Rizvi, senior vice president, Marsh

“But does it solve the problem of overcapacity? We don’t think so,” said Rizvi.

What may help is for the number of relatively newer ships that are scrapped each year to continue or even increase. Another crucial step will be to effectively manage both the skill sets and “culture capital” among combined crew and ship management that can be disturbed or disappear outright when companies merge.

“If you’re merging two shipping companies you want to make sure that their respective HR groups have a synergy and understand each other, put together one team that understands the needs of each of their vessels, their routes, their customers and the ports they call in,” he said.

Rizvi said some companies might consider another option: conversion from cargo to other lines of business. Shipyards, for example, said Rizvi, can’t build cruise ships quickly enough to meet demand. Very different from cargo, of course, but if it makes economic sense, why not?

Another opportunity is conversion to LNG, which is expected to thrive over the next several years with rising demand in clean energy resources.

Bigger Ships, More Complex Cargo

But the issue for Joe Sheridan is what happens if more companies like Hanjin go under, specifically claims being filed for warehouse forwarding charges to pay for discharge of cargo at dockside, temporary warehousing and a replacement vessel to get cargo to its original destination.

“That’s where the claims are really going to come into play,” said the marine specialist at Lockton cargo and logistics. How insurance policies are written will be critical to how well container shippers fare going forward, he said.

Some underwriters, for example, attach sublimits to liabilities for a single occurrence. A bigger issue, said Rizvi and Sheridan, is the stipulation in some policies that each bill of lading be insured separately, in which case multiple deductibles would apply in exigent circumstances.

Continued reliance on megaships with their massive cargo loads and numerous clients poses an obvious challenge here, said Sheridan.

Continued reliance on megaships with their massive cargo loads and numerous clients poses an obvious challenge here, said Sheridan.

“If you go out and put a $10 million limit on one cargo account and a $20 million limit on another, you don’t know how many cargo accounts you have exposure to on one vessel because these ships are so big. There’s no way they can determine that.”

Bottom line, there’s an array of marine cargo insurance policies out there written along a broad spectrum of terms and conditions and it will be up to individual underwriters to determine how language changes or stays the same going forward.

Some underwriters and clients weren’t really hit very hard after Hanjin went under while others were, said Sheridan. But changes are definitely afoot.

“They’re asking, ‘Is this something that could happen again?’ I’ve been in this business for over 20 years and I’ve never seen anything happen of this scale and magnitude. Our argument is that shippers should take a hard look at these policies before these things happen.”

Still at Sea Over Low Demand

Blaeser was happy to see consolidation continue apace since his company’s report a year ago, notably the joint announcement that Mitsui O.S.K. Lines, Nippon Yusen and Kawasaki Kisen Kaisha are merging their container shipping businesses this July to begin operations in April 2018.

Overall, the industry will enjoy stable business from higher, compensatory freight rates as fewer hands control the capacity side, said Blaeser, while “the benefits to the manufacturers and retailers that rely on their services will be decreased volatility and more reliability in terms of services.”

“But with consolidation we’re still not out of the woods,” Blaeser added. “If fewer hands don’t manage the global fleet in a tighter manner, then those benefits won’t happen.”

Non-market forces, too, “have weighed on the market to the detriment of the ocean carrier business,” said Blaeser. Governments, in particular Asian governments, have backed companies unable to make it on their own — neglecting one crucial economic factor: global demand.

“If governments, be they American or European or wherever, reverse track on their trading policies then that will inevitably hit demand ferociously,” Blaeser said. “Where demand might be threatened, the industry absolutely has to take it seriously.” &