Recent Events

Risk Matrix

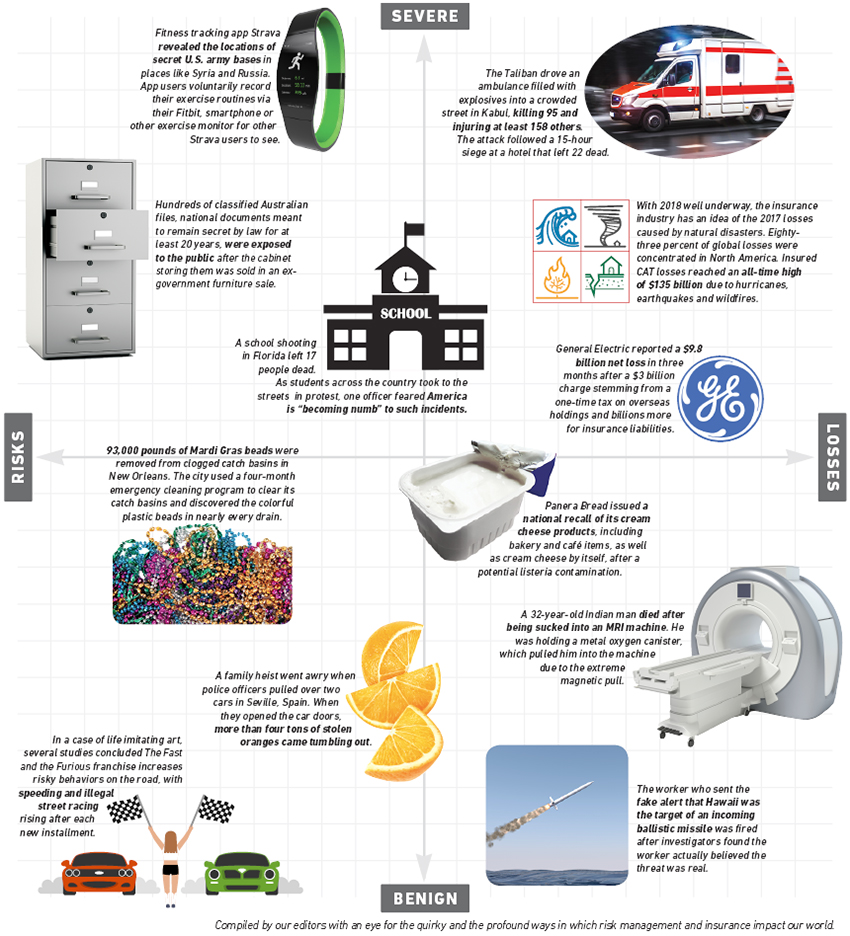

Quirky and profound ways in which risk management and insurance impact our lives.

White papers, service directory and conferences for the R&I community.