Insurance Agency M&A Market Settles Into New Normal as Consolidation Accelerates

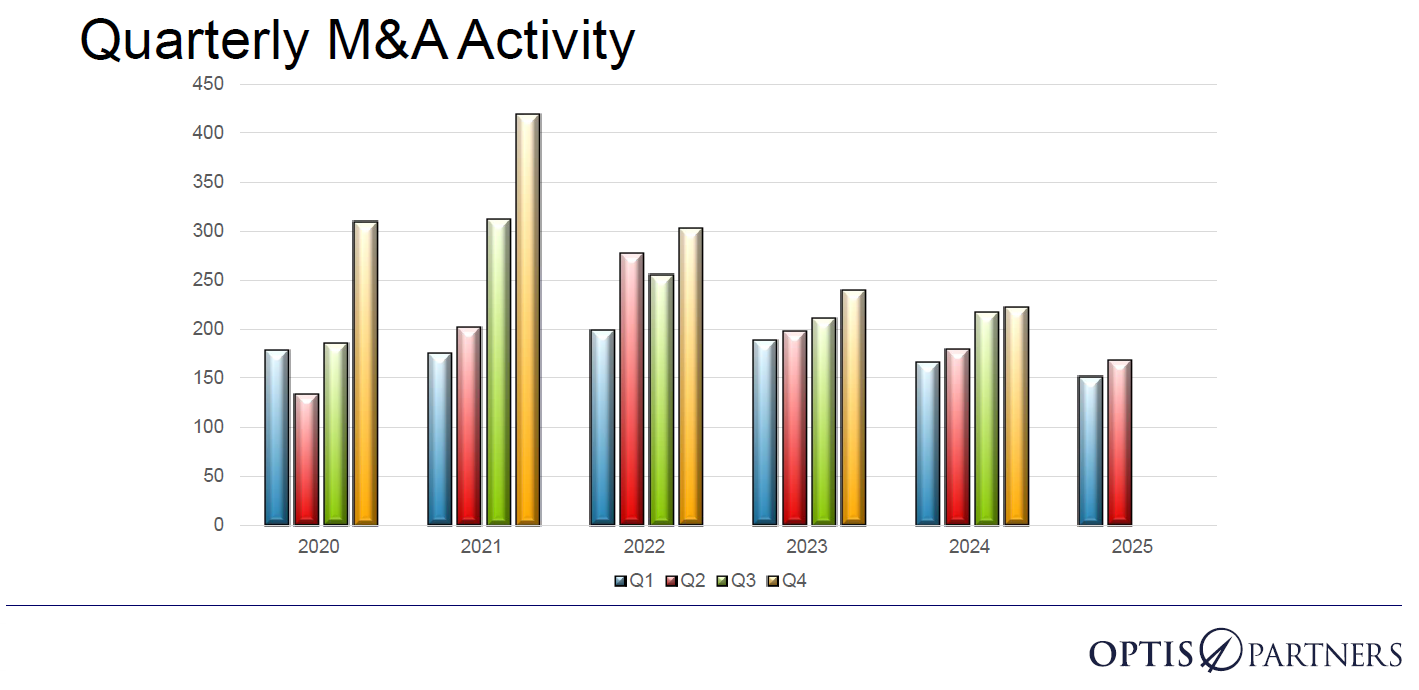

The insurance agency merger and acquisition market completed 319 transactions during the first half of 2025, reflecting an 8% decline from the same period last year, according to a first-half 2025 analysis by OPTIS Partners.

The insurance agency M&A landscape has found a new rhythm, according to the report, as the industry settles into a new normal of 750-800 deals per year, while accelerating consolidation reduces the buyer pool. The new pace follows the unprecedented activity of 2021 and 2022, when acquisitions totaled 1,108 and 1,032, respectively.

Deal flow reached 758 transactions over the past 12 months, maintaining the consistent pace established since the fourth quarter of 2023. Second quarter 2025 saw 168 announced deals, representing an 11% increase from the previous quarter despite being 6% below the same period last year and 15% below the five-year average, OPTIS Partners said.

Private equity-backed and hybrid buyers continue their market dominance, accounting for more than 72% of all announced transactions in both the past 12 months and most recent quarter, according to the report. These firms consistently close approximately 70% of total quarterly deals since the pandemic began.

The investor category has expanded beyond traditional private equity to include what OPTIS Partners terms “Private Equity-Hybrid” buyers, encompassing institutional capital investors such as family offices, pension funds, and sovereign wealth funds entering the market for the first time.

BroadStreet Partners maintains its position as the most active acquirer with 39 transactions in the first half of 2025, followed by Hub International with 27 deals and Inszone Insurance Services with 18 transactions. On a trailing 12-month basis, BroadStreet Partners leads with 80 deals, 39% above its five-year average, while Hub International follows with 62 deals, per the report.

Shifting Dynamics Create Opportunities and Challenges

The market demonstrates divergent momentum among major players (those with 20 or more deals over the past 12 months), with some firms accelerating their acquisition pace while others pull back. King Risk Partners increased M&A activity in the first half by 160%, HighStreet Partners grew by 55%, and World Insurance Associates expanded by 26% among the most active buyers, the report said.

Conversely, several established acquirers have reduced their transaction volume. Patriot Growth Insurance Services decreased activity by 32%, Inszone Insurance Services by 24%, Arthur J. Gallagher by 23%, and Acrisure by 15% compared to their previous pace.

The buyer landscape reveals significant consolidation pressure, according to OPTIS Partners. Privately owned buyers completed 142 deals in the past 12 months, representing 19% of first-half 2025 transactions, maintaining similar proportions to the previous year despite the overall market contraction.

Large-scale transactions continue to shape the industry, with notable deals including Gallagher’s expected $2.9 billion acquisition of AssuredPartners and Brown & Brown’s anticipated $1.7 billion purchase of Accession Risk Management, both expected to close in the second half of 2025.

Industry Consolidation Accelerates Despite Fewer Overall Deals

The insurance agency M&A market reflects accelerating consolidation even as total transaction volume remains below historical peaks, the report noted. The number of unique buyers dropped dramatically from 140 in 2020 to 99 in the first half of 2025, while the 10 most active buyers increased their market share to 54% of deals currently from 44% of deals in 2020.

This consolidation trend appears positioned to continue. The report anticipates deal flow will remain in the 750-800 annual range while larger firms pursue bigger transactions to fuel necessary growth. The shrinking buyer pool suggests some of today’s active acquirers may become tomorrow’s sellers as the industry matures.

View the full report here. &