Claims

A Glut of Medical Causation Claims

So called “cappers” or “runners,” who are middlemen in fraud schemes, are illegally recruiting recently unemployed workers to file murky medical-causation allegations, helping to drive a surge in Southern California workers’ compensation cases.

“We are getting slammed with really unscrupulous lawyer-developed cases,” said Robert G. Rassp, a Southern California claimant attorney and author of the law blog “The Rassp Report.”

“They add in their claim not just the back injury, but psychiatric claims, sleep disorder and sexual dysfunction. They throw the whole book at the employer. Risk managers are going berserk over it.”

The participants in such schemes take advantage of California’s workers’ comp causation standards allowing the filing of cumulative trauma injury claims after a worker has been terminated, Rassp said. California further allows compensation when the causation is less than 1 percent work-related.

Even without the involvement of cappers, California’s liberal causation standards create headaches for employers in terms of apportioning between industrial and non-industrial factors behind post-termination cumulative trauma claims.

“We have a huge problem with this,” said a Southern California risk manager who asked not to be identified.

California’s laws are just one issue currently fueling more nationwide discussions about medical causation standards and the challenge of determining whether workplace exposures are responsible for specific cumulative trauma claims.

Robert Rassp, claimant attorney

Claims-payer desire for more states to adopt stricter injury-causation standards along with the shifting nature of jobs and worker demographics are also stirring those discussions.

Claims with questionable medical-causation assertions have always presented a conundrum for payers: Failing to challenge cases when the injury cause is not work-related leads to paying unwarranted benefits and emboldens others to file similar spurious cases.

Wrongly challenging claimants, on the other hand, when their medical conditions legitimately arise from work, can needlessly drive litigation costs, with the severity of those expenses depending on state statutes.

In Pennsylvania, for example, claims payers lacking a reasonable basis for contesting an injured worker’s petition may be ordered to pay the claimant’s lawyer fees and litigation costs, said Michael D. Sherman, a defense attorney at Chartwell Law Offices LLP in Pittsburgh.

Determining causation is easier when an obvious workplace accident, with witnesses, causes an easily identified injury like a severed finger or broken bone.

But with a cumulative trauma injury or chronic problem occurring over time, such as an inflamed shoulder or lower-back pain, confirming unequivocally that it arose during the course of employment challenges employers, injured workers and even doctors.

Doctor training focuses on treating injuries, not on uncovering their cause, said Nancy Greenwald, a Boise, Idaho-based physician who treats workers’ comp patients.

“It’s one of the hardest things we do as physicians to really pinpoint what caused that particular injury,” she said.

Throw in the possibility of pre-existing conditions or an injury aggravation occurring after the industrial harm and making the right judgment call regarding the payer’s responsibility is even trickier.

While such scenarios present a challenge in determining the scope of legitimate claims, the schemers utilizing cappers in Southern California willfully take advantage to perpetuate fraud.

Last year, for example, a San Diego grand jury indicted doctors, medical providers and attorneys allegedly participating in a scheme involving cappers and $450,000 in illegal kickbacks.

Prosecutors allege it generated millions of dollars of fraudulent workers’ comp claims.

Other cappers have been busy in Southern California’s Orange and Los Angeles counties, soliciting workers who recently lost their jobs due to plant closings or other factors, Rassp said.

Rassp is alarmed by the practice because it increases claims payer suspicions, driving them to challenge more cases even when causation is legitimately work-related, he said.

Workers validly harmed on the job pay the price.

“If the problem is employment-related, deal with that.”– Stuart Colburn, a defense attorney at Downs Stanford P.C in Austin, Texas

A “glut” of post-termination cumulative trauma claims filed in Southern California perplexes employers who may delay benefit payments and create unwarranted friction with legitimately injured workers when they attempt to protect themselves, agreed Edward E. Canavan, vice president of the workers’ comp practice and compliance at Sedgwick Claims Management Services.

“It’s unfortunate,” because injured workers have families to care for, Canavan added.

The workers’ comp industry needs to consider legislative and regulatory changes to curb Southern California abuses while continuing to pay legitimate claims, Canavan said.

Nationwide, increased discussions about causation standards come after a number of states raised the level of medical evidence required to prove a work-related injury, said Thomas A. Robinson, co-author of “Larson’s Workers’ Compensation Law.”

“There are at least a half dozen states that over the past decade and a half made it more difficult for the claimant to prove their case based on requiring more definite medical opinions,” Robinson said.

Debra Levy, SVP, York Risk Services Group

While implementation of those laws “has sort of snuck up on people,” claimant representatives are increasingly complaining about them while claims payers want legislatures in more states to adopt similar legislation.

Greg McKenna, senior vice president for external affairs at Gallagher Bassett, expects more states to consider reforms with strengthened causation standards.

But passage of such laws probably will depend on balancing them with increased benefit amounts, he said.

“I really think lawmakers and employers are wrestling with a new kind of workforce,” McKenna said.

In the past, when workers remained at a single job for years, employers could more easily accept workplace responsibility for cumulative trauma, McKenna said.

But with workers frequently changing jobs, and perhaps even working a second job in the “gig-economy,” employers are asking whether they should accept cumulative-trauma injuries that workers may have acquired during previous employment.

Similarly, an older U.S. workforce raises questions about whether injuries are work-related or stem from age-related continuous degenerative processes.

The aging workforce, general increase in co-morbid conditions and uncertainty over group health make it more important than ever for payers to confirm that alleged injuries actually resulted from workplace accidents, said Maureen McCarthy, senior vice president, workers’ compensation claims, at Liberty Mutual.

Meanwhile, a U.S. Department of Labor report released in 2016 reviewed the impact of state laws with stricter causation standards that increased the burden of proof required for claimants to prove a workers’ comp claim, Robinson noted.

The report said that “issues of causation of injury or illness have always presented challenges.”

It added that “there is substantial cause for growing alarm,” because of increasingly complex challenges workers face with new causation standards requiring work to be the major contributing cause of disabilities.

Observers fret that the DOL’s report will drive federal intervention in state workers’ comp programs.

That still leaves the common challenge of filtering out other injury causes from workplace causation. The number of cases presenting those challenges can shift.

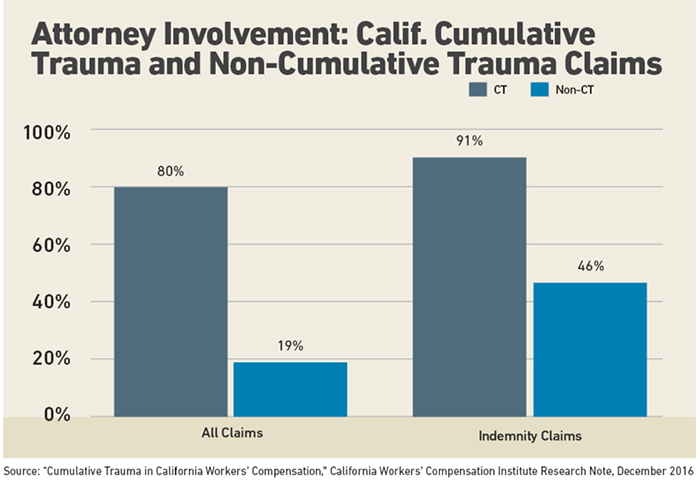

For full report: www.cwci.org/store.html

The Texas Department of Insurance, for example, has seen an increase in injured workers challenging the findings of designated doctors. They are requesting a “causation analysis” to determine issues such as maximum medical improvement, impairment rating, and extent of injury, a TDI spokesman said.

The department has not determined why more causation challenges are occurring.

But defense attorney Stuart Colburn at Downs Stanford P.C. in Austin said claimants have grown smarter at meeting requirements for challenging doctor findings that determine issues such as the extent of injury and return-to-work ability.

Mitigating claims with questionable causation issues calls for employers to identify the problem’s origin, Colburn said.

Employers experiencing multiple, unwitnessed, soft-tissue injuries should take a “big-picture approach” to learn, for example, if issues such as problematic employer/employee relations or the frequent assigning of unpleasant tasks is driving claim filings, he advised.

“If the problem is employment-related, deal with that,” Colburn said.

Return-to-work programs can help reduce unwarranted claims when workers realize they will be assigned other tasks rather than receiving time off, Colburn said.

Do not allow claims examiners to become jaded and assume a battle is lost when a jurisdiction’s laws, such as California’s, frequently work against favorable outcomes, said Debra Levy, senior vice president of product management and national workers’ comp practice leader at York Risk Services Group.

“Adjusters shouldn’t say, ‘That’s just the way the state is,’ without thoroughly investigating a claim,” she said. &