Global Commercial Insurance Rates Drop 2%, US Rates Flat in Q4 2024

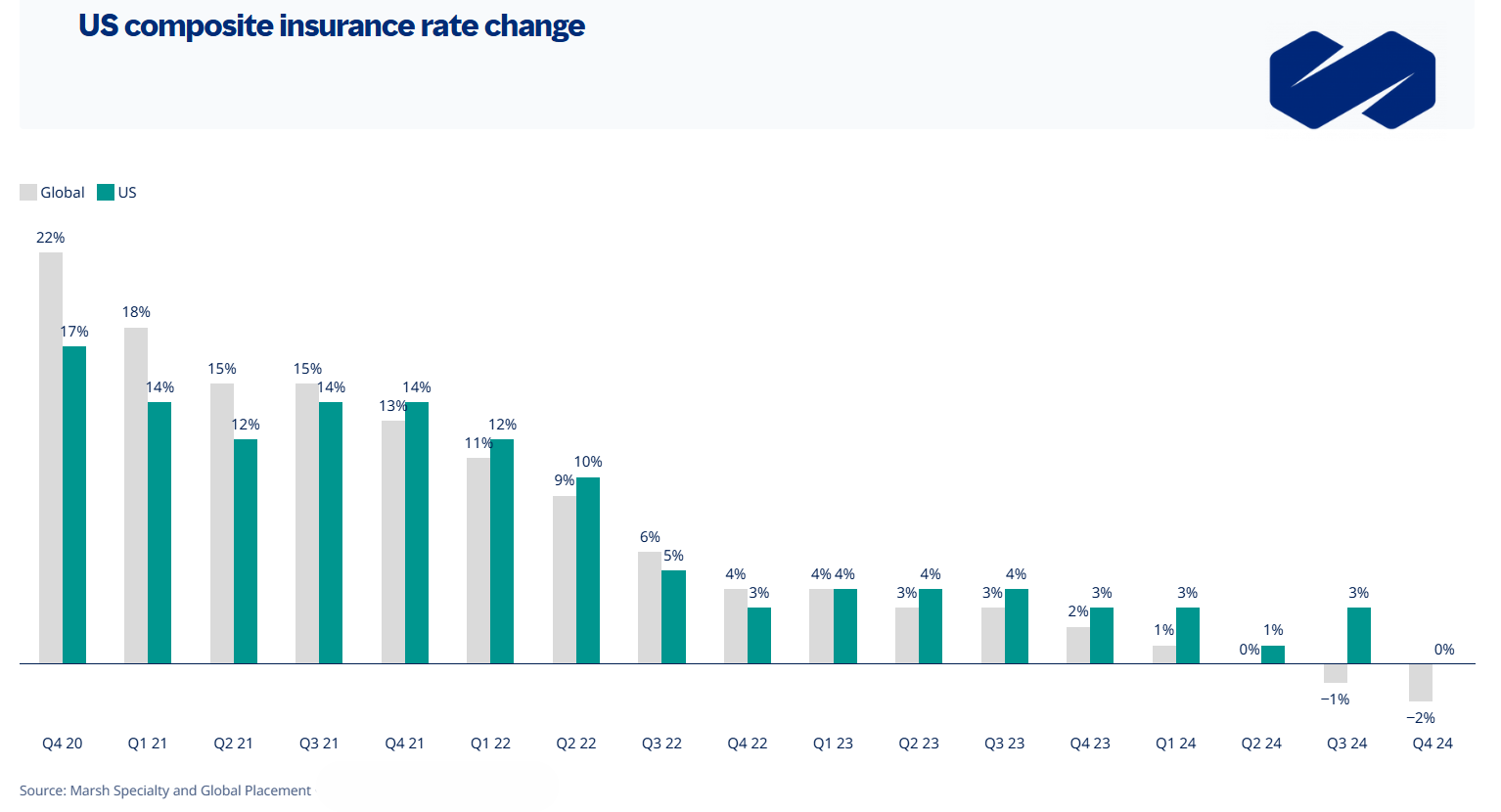

Global commercial insurance rates experienced a notable shift in the fourth quarter of 2024, declining by 2% on average, marking the second consecutive quarterly decrease following a prolonged period of seven years of consistent increases, according to Marsh’s Global Insurance Market Index for 2024.

The reversal in this long-standing trend signals a potentially significant turning point in the commercial insurance market landscape, with varying impacts expected across regions and coverage types.

“The softening of rates across property, financial lines and cyber are a positive development for clients, while the challenges in other areas of the market, particularly in U.S. casualty, are acute,” stated John Donnelly, global head of placement for Marsh.

The global commercial insurance landscape witnessed significant regional variations in the fourth quarter of 2024. The United Kingdom and Pacific regions led the pack with the most substantial rate decreases, experiencing drops of 5% and 8% respectively. This marked decline contrasted sharply with other parts of the world, where rates either remained stable or saw increases.

In the United States, insurance rates held steady, neither rising nor falling during this period. However, other regions painted a different picture. Latin America, the Caribbean, and the India, Middle East, and Africa (IMEA) region all bucked the trend, recording increases in their composite rates.

Product Line Performance Globally

Diving deeper into specific insurance lines reveals a mixed bag of global trends. Property insurance rates declined by 3% on average worldwide, slightly outpacing the previous quarter’s 2% decrease. This downward trend suggests a softening market for property coverage across the globe.

Casualty insurance emerged as the outlier among major coverage lines, being the only one to register an increase globally. Rates in this sector rose by 4% on average, though this increase was less pronounced than the 6% uptick observed in the preceding quarter. The persistent growth in casualty rates points to ongoing challenges and risk factors in this particular segment of the insurance market.

Financial and professional lines experienced a more significant downturn, with rates decreasing by 6% globally. This decline was consistent across all regions, indicating a widespread easing of rates in this sector.

Cyber insurance, a relatively newer but increasingly important line of coverage, saw rates decline by 7% in the fourth quarter. This decrease was observed uniformly across all regions, suggesting a global trend towards more competitive pricing in the cyber insurance market.

U.S. Market Deep Dive

Property Insurance: The U.S. property insurance market experienced a notable shift in the fourth quarter of 2024, with rates declining by 4% on average, a steeper drop compared to the 1% decrease observed in the previous quarter. This downward trend can be attributed to several factors, including increased insurer capacity and heightened competition within the sector.

Insurance companies, buoyed by strong financial performance in the property sector over the past three years, have begun to demonstrate greater underwriting flexibility. This shift has led to more favorable conditions for insureds, particularly in areas such as sub-limits, coverage definitions, and natural catastrophe deductibles.

Casualty Insurance: While property insurance rates declined, the casualty insurance market in the U.S. faced its own set of challenges. Overall, casualty rates increased by 7% in the fourth quarter, a slight moderation from the 10% rise seen in the third quarter. However, when excluding workers’ compensation, the average casualty rate increase was a more substantial 11%.

Workers’ compensation remains a primary focus for most insurers, but concerns are mounting regarding increasing reserves and rising medical costs. Additionally, auto liability continues to pose profitability challenges for insurers, largely due to larger jury verdicts nationwide and escalating auto physical damage costs.

Umbrella and Excess Liability: The umbrella and excess liability market saw significant rate increases, though the pace of growth has slowed. Risk-adjusted rates in this sector rose by 15% in the fourth quarter, down from 21% in the previous quarter. However, clients with adverse loss development and exposure concerns faced even steeper rate hikes, often exceeding 30%.

These substantial increases are prompting many clients to explore alternative risk financing solutions, such as captives and structured deals, as they seek to manage their insurance costs more effectively.

Financial and Specialty Lines: The financial and professional lines insurance market experienced a notable shift in the fourth quarter of 2024, with rates decreasing by 3% overall. This decline was consistent across various specialty lines, though the magnitude varied.

Directors and officers (D&O) liability insurance saw the most significant drop, with rates declining by 5%. This decrease suggests a softening market for executive protection coverage, potentially due to increased competition among insurers or improved risk profiles of insured companies.

In contrast, fiduciary liability insurance rates remained relatively stable, showing no significant change during the quarter. This stability might indicate a balanced market for pension and employee benefit plan coverage.

Errors and omissions (E&O) insurance bucked the downward trend, with rates increasing by a modest 1%. This slight uptick could reflect ongoing concerns about professional liability risks in various industries.

Financial institution (FI) insurance rates decreased by 2%, aligning with the overall downward trend in the financial and professional lines sector. This reduction may signal improved risk management practices within the financial services industry or increased capacity in the insurance market.

Cyber Insurance: The cyber insurance market also saw significant changes in the fourth quarter of 2024. Rates in this specialized line decreased by 5%, marking a notable shift from the sharp increases observed in recent years.

This rate reduction coincides with abundant capacity in both primary and excess cyber insurance programs. The increased availability of coverage options suggests that insurers may be growing more comfortable with their ability to assess and price cyber risks accurately.

View the Marsh report here. &