Excess/Surplus

Buyer Beware

The steep slopes of the Rocky Mountains and the Pacific Northwest are prime real estate. But they also host an increasingly dangerous risk: landslides.

Landslides wreak, on average, $1 billion to $2 billion worth of damage to properties every year, destroying buildings, roads, power lines, pipelines and even entire neighborhoods.

Mudslides, one of the most common types of landslide, are caused by extreme rainfall, earthquakes, wildfires and man-made disasters. They can strike quickly and they have increased in both severity and frequency in recent years.

Among the worst affected regions are the Appalachian Mountains in the East, the central Rocky Mountains and the western Pacific Coastal Ranges. These are home to steep and hilly areas that suffered from years of drought, experienced forest fires and then got pummeled by flash flooding.

Jonathan Godt, program coordinator, U.S. Geological Survey

One of the deadliest mudslides in U.S. history was in Oso, Wash., in 2014. That slide was caused partly by logging activities in the area. When a denuded hill collapsed after weeks of rain, the resulting slide killed 43 people and destroyed 49 homes.

Most at risk are mining and logging companies with extensive operations at mountain bases and valleys in areas prone to heavy rainfall, flooding and earthquakes.

“Most of the landslides in the U.S. over the last 25 years have been driven by rainfall,” said Jonathan Godt, program coordinator at U.S. Geological Survey (USGS).

“A combination of steep topography, abundant material on the mountainsides and heavy rainfall all converge to create the perfect storm.

“With a growing population and less space in the cities, more people are moving home or business to the mountains and are putting themselves and their properties in harm’s way, thus increasing the likelihood of landslides.”

Mudslide vs. Mudflow

Gary Marchitello, head of property for North America at Willis Towers Watson, said that mudslides are primarily caused by excessive rainfall or snowpack on a slope, or an earthquake.

“A mudslide, by definition, implies that gravity has a part to play,” he said.

“The soil is loosened by the rain or snow, or the ground shaking, and gravity does the rest.”

Marchitello said that it was important to make the distinction between mudslides and mudflow, which is caused by river overflow and would typically be covered under standard flood insurance.

“If you have either flood coverage as part of an all risk policy or you buy it as a stand-alone peril, you should be covered for mudflow,” he said.

Coverage for damage from mudslides, however, doesn’t come as standard and requires a separate earth movement policy or difference in conditions coverage from a specialty insurer.

“Clearly, if there was a seismic event that caused a movement of earth to slide down the mountain, that would be covered under these separate policies, said Marchitello.

“But then there are other circumstances where you get an excess of rain or snowfall, which may not necessarily have anything to do with the earth shaking, in which case it could fall into earth movement or flood, depending on the approximate cause.”

Duncan Ellis, U.S. property practice leader, Marsh

Where a mudslide or mudflow occurs because trees and plants were damaged in an earlier fire and the area had never previously experienced flooding or mud problems, most properties will be covered as a fire loss, he added.

Duncan Ellis, U.S. property practice leader at Marsh, said that it is important to first establish if and how mudslides are covered under an all risk policy.

“You need to read your policy carefully and understand what you are covered for, if at all, in terms of earthquake, earth movement and flood because there are a lot of nuances,” he said.

“If you have a policy that has earthquake cover, for example, I would argue mudslides and mudflows would not be covered.”

Cindy Collins, assistant vice president and program manager for alternative markets at Zurich North America, said that most E&S insurers prefer to limit additional coverage to earthquake, however, they may choose to include earth movement such as landslide, mine subsidence and earth sinking, depending on the circumstance.

“When the decision is made to provide the additional coverage, it would likely have a sublimit to apply, anywhere from $1 million to $25 million or more,” she said.

Identify and Assess Potential Magnitude of Mudslides

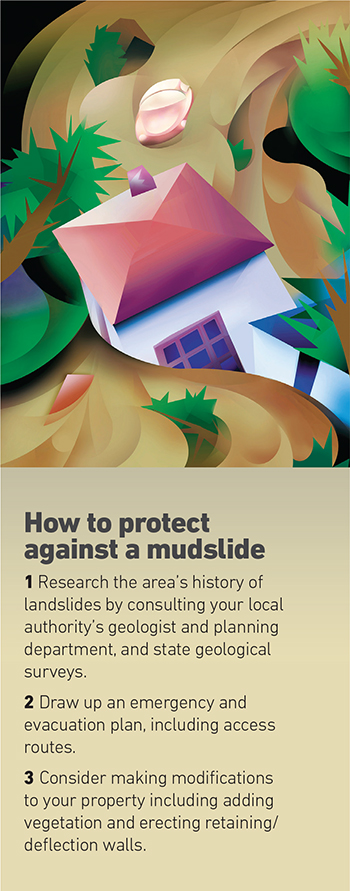

Marchitello said that risk managers and companies first need to identify and assess the potential magnitude of any mudslides before coming up with a risk mitigation plan.

A good resource for this, he said, is the USGS and Federal Emergency Management Agency (FEMA), which provides advice on mudslides. He also recommends enlisting the help of a civil engineering firm.

Counties affected by mudslides also carry out hazard mitigation planning and zoning, while at a state level there are geological programs, surveys and geologists available, he said.

“Clearly if you own a property at the base of a mountain you would think there is potentially a risk of a mudslide,” said Marchitello.

“Clearly if you own a property at the base of a mountain you would think there is potentially a risk of a mudslide,” said Marchitello.

“Then it’s a case of carrying out your own investigation using techniques such as satellite imagery and looking at past events.”

Perhaps most importantly, companies should have an emergency and evacuation plan in place in the event of a disaster, added Marchitello.

“Short of moving your operation, there is very little you can do, however, to protect your property from a catastrophic event,” he said.

Michael Barry, vice president of media relations at the Insurance Information Institute, said that companies also need to look closely at land surveys and the property’s claims history.

“Risk managers must assess land surveys and the claim-filing histories of the properties their clients plan either to purchase, or operate their businesses on,” he said.

In terms of physical modifications to property, Timothy Chaix, president of R.E. Chaix & Associates, advised that businesses can add vegetation, or erect deflection barriers or retaining walls to divert a mudslide.

However, he warned that they would be liable if the diverted mud caused damage to a neighboring property.

“Right now, there is a tremendous amount of rain, particularly in California, and the area has become much more vulnerable to mudslides and earth movement because the ground was so dry before so it is not able to soak up the water as easily,” he said.

Landslides Being Added to Earthquake Models

Landslides have become so frequent and severe that modelers are making adjustments.

Dr. Jayanta Guin, chief research officer at AIR Worldwide, said that the risk modeling firm recently added landslides into its earthquake model for Canada with plans to incorporate a similar component into its U.S. model this year.

The new module will cover the 48 mainland states and model damage caused by landslides resulting from earthquake ground shaking.

“Landslide risk is calculated based on a combination of slope information derived from Digital Elevation Model data, surficial and bedrock geographical features that determine how well the slope resists failure, and soil wetness, which varies depending on the time of year,” he said.

“The probability of a landslide actually occurring is then calculated based on the level of ground shaking.”

RMS also models the risk of landslides within its earthquake models.

“These models provide a landslide susceptibility class that is defined by local soil properties and the slope angle,” said Ben Reynolds, RMS specialist in earth sciences and earthquake modeling.

“This information can be used to identify more vulnerable locations, and would be automatically included as part of the earthquake risk modeling where we have identified significant risk of landslides.”

Wes Anderson, national property president at Risk Placement Services, said that combining mapping and working with FEMA to determine the property’s designated flood zone and elevation, enables businesses to decide on the appropriate insurance coverage and limits.

“The most valuable coverage you can buy is loss avoidance, especially when the catastrophic peril of landslide is the cause for discussion,” he said. &