Sponsored: Liberty International Underwriters

A Renaissance In U.S. Energy

America’s energy resurgence is one of the biggest economic game-changers in modern global history. Current technologies are extracting more oil and gas from shale, oil sands and beneath the ocean floor.

Domestic manufacturers once clamoring for more affordable fuels now have them. Breaking from its past role as a hungry energy importer, the U.S. is moving toward potentially becoming a major energy exporter.

“As the surge in domestic energy production becomes a game-changer, it’s time to change the game when it comes to both midstream and downstream energy risk management and risk transfer,” said Rob Rokicki, a New York-based senior vice president with Liberty International Underwriters (LIU) with 25 years of experience underwriting energy property risks around the globe.

Given the domino effect, whereby critical issues impact each other, today’s businesses and insurers can no longer look at challenges in isolation one issue at a time. A holistic, collaborative and integrated approach to minimizing risk and improving outcomes is called for instead.

Aging Infrastructure, Aging Personnel

Robert Rokicki, Senior Vice President, Liberty International Underwriters

The irony of the domestic energy surge is that just as the industry is poised to capitalize on the bonanza, its infrastructure is in serious need of improvement. Ten years ago, the domestic refining industry was declining, with much of the industry moving overseas. That decline was exacerbated by the Great Recession, meaning even less investment went into the domestic energy infrastructure, which is now facing a sudden upsurge in the volume of gas and oil it’s being called on to handle and process.

“We are in a renaissance for energy’s midstream and downstream business leading us to a critical point that no one predicted,” Rokicki said. “Plants that were once stranded assets have become diamonds based on their location. Plus, there was not a lot of new talent coming into the industry during that fallow period.”

In fact, according to a 2014 Manpower Inc. study, an aging workforce along with a lack of new talent and skills coming in is one of the largest threats facing the energy sector today. Other estimates show that during the next decade, approximately 50 percent of those working in the energy industry will be retiring. “So risk managers can now add concerns about an aging workforce to concerns about the aging infrastructure,” he said.

Increasing Frequency of Severity

Current financial factors have also contributed to a marked increase in frequency of severity losses in both the midstream and downstream energy sector. The costs associated with upgrades, debottlenecking and replacement of equipment, have increased significantly,” Rokicki said. For example, a small loss 10 years ago in the $1 million to $5 million ranges, is now increasing rapidly and could readily develop into a $20 million to $30 million loss.

Current financial factors have also contributed to a marked increase in frequency of severity losses in both the midstream and downstream energy sector. The costs associated with upgrades, debottlenecking and replacement of equipment, have increased significantly,” Rokicki said. For example, a small loss 10 years ago in the $1 million to $5 million ranges, is now increasing rapidly and could readily develop into a $20 million to $30 million loss.

Man-made disasters, such as fires and explosions that are linked to aging infrastructure and the decrease in experienced staff due to the aging workforce, play a big part. The location of energy midstream and downstream facilities has added to the underwriting risk.

“When you look at energy plants, they tend to be located around rivers, near ports, or near a harbor. These assets are susceptible to flood and storm surge exposure from a natural catastrophe standpoint. We are seeing greater concentrations of assets located in areas that are highly exposed to natural catastrophe perils,” Rokicki explained.

“A hurricane thirty years ago would affect fewer installations then a storm does today. This increases aggregation and the magnitude for potential loss.”

Buyer Beware

On its own, the domestic energy bonanza presents complex risk management challenges.

However, gradual changes to insurance coverage for both midstream and downstream energy have complicated the situation further. Broadening coverage over the decades by downstream energy carriers has led to greater uncertainty in adjusting claims.

A combination of the downturn in domestic energy production, the recession and soft insurance market cycles meant greatly increased competition from carriers and resulted in the writing of untested policy language.

In effect, the industry went from an environment of tested policy language and structure to vague and ambiguous policy language.

Keep in mind that no one carrier has the capacity to underwrite a $3 billion oil refinery. Each insurance program has many carriers that subscribe and share the risk, with each carrier potentially participating on differential terms.

“Achieving clarity in the policy language is getting very complicated and potentially detrimental,” Rokicki said.

Back to Basics

Has the time come for a reset?

Has the time come for a reset?

Rokicki proposes getting back to basics with both midstream and downstream energy risk management and risk transfer.

He recommends that the insured, the broker, and the carrier’s underwriter, engineer and claims executive sit down and make sure they are all on the same page about coverage terms and conditions.

It’s something the industry used to do and got away from, but needs to get back to.

“Having a claims person involved with policy wording before a loss is of the utmost importance,” Rokicki said, “because that claims executive can best explain to the insured what they can expect from policy coverage prior to any loss, eliminating the frustration of interpreting today’s policy wording.”

As well, having an engineer and underwriter working on the team with dual accountability and responsibility can be invaluable, often leading to innovative coverage solutions for clients as a result of close collaboration.

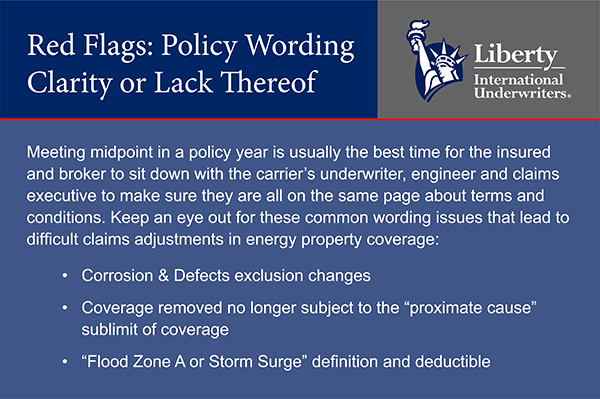

According to Rokicki, the best time to have this collaborative discussion is at the mid-point in a policy year. For a property policy that runs from July 1 through June 30, for example, the meeting should happen in December or January. If underwriters try to discuss policy-wording concerns during the renewal period on their own, the process tends to get overshadowed by the negotiations centered around premiums.

After a loss occurs is not the best time to find out everyone was thinking differently about the coverage,” he said.

Changes in both the energy and insurance markets require a new approach to minimizing risk. A more holistic, less siloed approach is called for in today’s climate. Carriers need to conduct more complex analysis across multiple measures and have in-depth conversations with brokers and insureds to create a better understanding and collectively develop the best solutions. LIU’s integrated business approach utilizing underwriters, engineers and claims executives provides a solid platform for realizing success in this new and ever-changing energy environment.

![]()

This article was produced by the R&I Brand Studio, a unit of the advertising department of Risk & Insurance, in collaboration with Liberty International Underwriters. The editorial staff of Risk & Insurance had no role in its preparation.