Is Your Insurance Company Ready for AI? Understanding the Pluses and the Pitfalls Before Adoption

Humor me with a quick reflective exercise: think about how you spent your weekends in October.

Perhaps you toured a haunted house, ordered a pumpkin spice latte, dined at a beer garden for Oktoberfest, ventured on an apple picking foray. Maybe you took a drive to witness the changing colors of the leaves or bought some new sweaters to guard you against the crisp fall chill.

I’m willing to bet you didn’t spend one weekend — let alone multiple — browsing the aisles of big box or specialty stores for Halloween costumes. You probably opened your laptop (or *gasp* your phone) and ordered one off Amazon. Next day delivery of course.

In recent years, humankind has embraced new technology after new technology. Now, as we enter the era of AI, companies are asking us to adopt yet another tool. And Prashant Hinge, chief transformation officer for MSIG USA, argues it should be as simple to take up as online shopping — especially for those in the insurance industry.

“In our personal lives, the time and cost of consuming goods and services has gone down exponentially. Similarly, what AI does is reduce the speed, reduce the time it takes for underwriters and adjusters to get more information so they can make an informed decision. This helps enhance efficiency and effectiveness at the same time,” Hinge said.

The ways in which AI could accelerate the insurance process are manifold. Underwriters can use it to sift through submissions and assess their quality. Adjusters can use it to review claims for fraud and predict their life cycles. In an industry beleaguered by talent shortages any tool that helps reduce workloads is welcome. The tool is extremely new, however, and insurers need to be mindful of the risks that come with embracing AI.

“AI is not the end of or be all, it is one of the tools in our toolbox that is extremely powerful,” Hinge said. “AI doesn’t work for everything. Any steps where there is human judgment involved, the industry experience to me that is still more relevant than AI. Hence designing the right balance for human and machine augmentation at speed and reasonable costs is important.”

The Major Applications of AI in Insurance

AI in insurance has two primary applications: underwriting and claims. “AI-based use cases should be carefully selected based on risk of execution and value, as they span across the insurance lifecycle,” Hinge said.

“We see the use of AI as an augmentation tool for every job family,” added Paul Drennan, chief data science officer for The Hartford. “Some applications are discrete to an insurance decision, like underwriting or claim handling. Others are more general and allow individuals to leverage AI at their desk to achieve greater productivity.”

On the underwriting end, “AI can now help you aggregate risk, aggregate pricing information, bring third-party data that is relevant for a specific risk, and present this to an underwriter to enable their decision,” Hinge said.

“It reduces manual labor,” added Zubair Shams, executive vice president of strategic analytics for Arch Insurance. “It can be applied to hundreds of thousands of submissions as they come in, that’s not someone sitting at their desk and keying in five prompts to get an answer or an insight.”

When AI tech reduces the manual labor of reviewing submissions, underwriters can direct their attention to crafting tailored policy solutions — something insureds will appreciate in today’s world where exposures have become more complex and ever-changing. “AI can help us differentiate in the marketplace and customize risk solutions for our global clients at scale,” Hinge said.

Insureds will also appreciate how much faster AI can make the insurance process. “It can reduce the number of questions that we ask our brokers,” Shams said. “It allows us to go back to the brokers more quickly and be more responsive to our markets.”

On the adjuster end, insurers can use AI to review documentation, like medical bills, and detect any issues a claim might encounter. “We see AI being used to identify some of those complex claims,” Shams said.

“You can look at fraud. You can look at predicting the cost. You can look at forecasting what the life cycle of a claim is going to look like,” Hinge added.

Lagging Behind or Moving too Fast?

Insurers, somewhat surprisingly, have been quick to embrace AI. A industry survey from Conning found that 77% of companies in the insurance sector were in the process of adopting AI into their processes. Part of the reason they’re rushing to adopt the tech? Cost. An individual insurance company’s revenue could increase 15 to 20% and their costs could reduce by five to 15% by using the tech, per April estimates from Bain & Company.

“We have a culture of really embracing new things,” Shams said of Arch’s approach to AI and other cutting edge tech. “We’ve spent seven plus years at this point on analytics and embracing it.”

Some may be swift to introduce AI because of concerns over the industry’s past reticence when it comes to technology. Insurers dragged their feet — sticking to paper files for years — and other industries surpassed them. They don’t want to make that mistake again. But as they sally to launch AI programs, some might be ignoring potential pitfalls.

“One of the biggest challenges in the industry is balancing the hype with reality,” Shams said.

One major problem: data quality. Insurers have historically been slow to embrace tech, so they may have unstandardized or incomplete data. AI systems are only as good as the data that goes into them. If you feed it a mess, it’ll spit out a mess.

“A lot of insurance carriers struggle with data quality,” Shams said. “It’s got the potential to have misleading results if we don’t start with the right strategy or the right approach to data.”

Poor data could also contribute to the hallucinations that are common with generative AI. Hallucinations are when AI makes up something — a citation, a fact, even a quote. These errors occur because of poor or incomplete training data, per a report from Google, or biases in the model. The amount AI makes stuff up varies — some models have hallucination rates as low as 3 percent. Others are as high as 27 percent, according to reporting from the New York Times. Do insurers really want to risk AI giving them a wrong result?

People can help mitigate some of this risk. AI can review submissions, but underwriters need to check the results and craft policies. They need to evaluate the models to make sure it isn’t producing biased results. Many of the experts interviewed for this story emphasized the important role people will play in safeguarding AI. That can reduce some of the risk posed by hallucinations.

“AI is still very good in narrow applications,” Hinge said. “AI might be getting better at replicating the functions of the human brain, but the ‘gut’ or judgment still requires the industry experience that is needed to make the best final decision.”

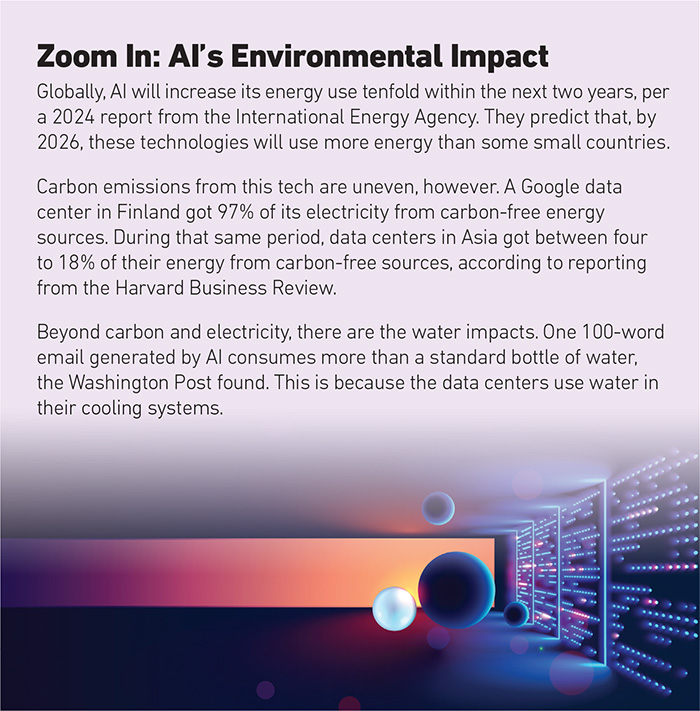

And there’s the environmental impact to consider, too. Yes, AI can help underwriters craft more complex and tailored policies, something that will be needed to manage new climate risks. But it’s also energy intensive.

Since they started developing AI systems, Google and Microsoft’s emissions have soared. Asking ChatGPT one question uses the same amount of electricity as running a lightbulb for 20 minutes, according to NPR. Insurers are among the companies that have made major commitments to reduce their emissions. Now the SEC is scrutinizing the climate pledges companies make. Where does AI fit in this picture?

“I don’t think we have identified the hidden or the unintended costs associated with AI yet, we are all learning real time,” Hinge said.

Governments are also looking to regulate AI technologies. The U.S. government has started drafting an AI bill of rights, which would protect people’s data and prohibit AI-based discrimination. Companies need to make sure they’re implementing these tools ethically.

“We have a very robust AI governance committee that evaluates various applications that come in and how it’s used,” Shams said.

Will People Accept AI?

Whether or not insurance companies are able to embrace AI as speedily as they’d like will largely come down to individual employees: will they accept or reject the technology?

“The last piece of adoption is how willing folks are to accept AI,” Shams said. “As with many technologies, we experience trepidations. There are questions like, ‘oh, is AI really going to replace me?’ ”

Experts say AI isn’t replacing adjusters or underwriters. It’s just augmenting their ability by automating some of the more tedious parts of their job so they can focus on developing creative insurance solutions.

“Nobody really wants to do the kind of work that’s monotonous,” Shams said. “[AI] allows our colleagues to focus on the things that they do best.”

Companies need to work with their employees to ensure buy-in for AI tools. If developers seek out different perspectives, they’ll be able to create AI tools with fewer biases.

“The most important aspect to properly embrace the technology is by bringing different groups together as part of the development process,” said Andrew Zarkowsky, head of AI underwriting at The Hartford. “That includes the business side, IT, data science, legal and compliance. It is not enough to understand AI or underwriting, we need individuals from all corners of our business that are deeply knowledgeable in both areas.”

Despite the potential risks associated with AI tech, many experts feel excited for how AI could transform insurance. AI presents exposures, but executives believe they can be managed with human oversight. The risk could be worth the financial reward, so the C-suite thinking goes.

“It’s really about empowering our employees, empowering our partners to do their jobs with more information, with more insights,” Shams said.

“AI is here. It’s going to be here for a long period of time,” Hinge added. “I feel hopeful that companies are innovating. We can do more with less and AI can help become the best version of ourselves.” &