Sponsored Content by AmTrust Financial

3 Ways a Data-Driven Warranty Model Better Protects Smart Home Technology

Technology has advanced in so many ways and so rapidly that for most of us, some modern-day tools seem lifted right out of a science fiction movie. We may not yet have transporters or replicators, but smart homes are the next best thing. The ability to lock doors, adjust the thermostat, dim the lights, turn on the oven or your favorite playlist from your smartphone is not only convenient, it’s simply cool.

It’s no surprise that the market for connected sensor technology is booming. According to Martech Advisor, 125 million devices will be connected through the Internet of Things by 2030, putting 15 connected devices into the hands of every consumer. According to the International Data Corporation, the global market for smart home technology is projected to grow at an annual compound rate of 16.9% through 2023, at which time more than half of American homes will be “smart” in some way.

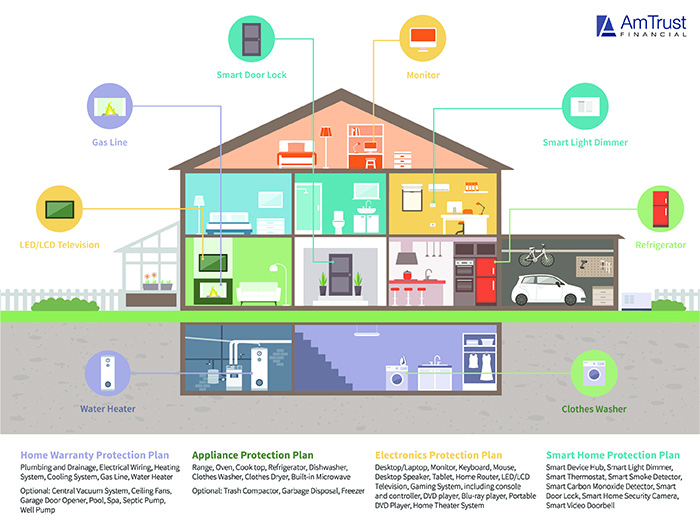

As demand for devices grows, so does the need for extended service warranties. Much of the sensor technology in homes today is easy to damage and expensive to fix.

“As people connect more devices to their homes, we’re seeing demand for more warranty packages that cover the entire smart home ecosystem,” said Aleem Lakhani, EVP, AmTrust Specialty Risk.

But the warranty packages that exist today don’t necessarily align with consumer needs or take advantage of the greatest benefit of connected devices — data.

What’s Wrong with Today’s Smart Home Warranties

Aleem Lakhani, EVP, AmTrust Specialty Risk

“We’re seeing the same approach taken with smart home systems as with all the other warranty products,” Lakhani said.

“The devices are treated as a bundle of products to be covered, without any regard to their uniqueness or the risk management practices of the user. You assume that a household has an ‘X’ number of devices, based on the national average, and you provide a certain bundle of coverage based on that assumption.”

This approach can grossly over- or underestimate the scale of a smart home system and the risk associated with it. Packages built this way do not adjust to the specific number or type of devices in a household, account for frequency of use, nor attempt to help customers get ahead of expensive repairs.

“Today when you go and purchase any consumer product from a big box retailer, notwithstanding your risk nature, you’re still awarded the same price as the customer behind you. It’s one size fits all,” Lakhani said.

Instead, smart home warranties should be predicated on the use of the data to inform a more dynamic solution. A data-driven warranty model is characterized by three traits: personalized, proactive and service-based. Here’s how it works:

1) Coverage Personalized to Unique Risk Profiles

Like an insurance policy, warranties are priced based on exposure to risk and the likelihood that repairs will be needed before the warranty expires. Unlike an insurance policy, warranties aren’t based on the individual consumer’s level of risk.

Think about the last time you purchased a warranty on a new piece of technology. Did anyone ask how often you plan to use the gadget, or for what purpose, or how many other devices the product would be interfacing with? Likely not.

Data from connected devices allow warranty underwriters to gather this information to craft more custom coverages without creating additional work for consumers. Discoverable connections within the household, for example, can tell warranty underwriters the true number of devices that require coverage, while usage data can indicate the likelihood of device failure.

“That allows us to be hyper accurate in identifying the nature of the products in the home and the risk associated with them. Data enables us to develop probability models around individuals and build warranties more commensurate with their risk,” Lakhani said.

2) Harnessing Data for Proactive Loss Prevention

This same data enables companies to spot potential trouble before costly repairs or replacements are needed, similar to the way manufacturers use telematics systems embedded in industrial machinery to identify the need for preventive maintenance.

“By having such rich information, we’re now able to engage in predictive analytics,” Lakhani said. “We’re able to identify particular scenarios that may result in failure or malfunction of a device and therefore be proactive in our engagement strategy, whether it be to inform the consumer about what they can do, dispatch a repair service, or facilitate a replacement before it’s necessary so that the consumer has a frictionless experience. That level of ease and convenience is what consumers today demand.”

The ability to predict repairs also enables service providers to achieve greater operational efficiency, budgeting for and preparing the relevant resources in greater alignment with expected outcomes.

“Empowered by data, we can do reverse logistical planning much more dynamically and therefore bring more economies to the end user,” Lakhani said.

3) Building a Warranty-as-a-Service Business Model

In addition to enabling more granular risk assessment and the power of prediction, data generated by sensor technology also makes it easier to track how risk changes over time. This creates the opportunity to break away from the traditional, full-pay warranty business model which estimates a cumulative risk level over the length of the contract.

Use-based and subscription models instead allow for variability in risk level as devices are added or removed from the home.

“The subscription model completely transforms the nature of a warranty from a product — a protection plan effective for a finite period of time — to a service, in which this protection is ongoing and grows and adapts along with the smart home ecosystem,” Lakhani said.

For consumers, this flexible model eliminates the complexities of knowing which devices are covered under which warranty. It also provides a channel through which consumers can access information about their product or connect with technicians.

This not only adds value to the warranty but also gives manufacturers and retailers more touch points with customers, building engagement and loyalty that can bring long-term financial benefit.

Breaking Barriers in Smart Home Insurance

One reason why the home warranty market lacks service-based, smart home package solutions is because most providers lack the capabilities needed to capture, clean and utilize data from disparate devices in private residences. Much of this effort is focused in the commercial marketplace.

AmTrust Specialty Risk is the first insurer to bring a service model to the smart home warranty market.

“We will continuously push the envelope of what the warranty industry looks like, largely because this is an overlooked area of risk,” Lakhani said. “Sensor technology is highly permeable, breaking down barriers between different sectors of life – home, health, auto, etc. — and creating voluminous data. That data and the devices that generate it need better protection than what’s available today.”

Along with its subscription warranty model, AmTrust is also working with top cybersecurity companies to bring breach detection and data privacy solutions to the consumer market. The result is a comprehensive protection plan covering every vulnerability in a smart home system.

“We have a rich tradition of being the first in offering new solutions to the market,” Lakhani said. “Within Specialty Risk, our executive leadership is highly engaged and invested in innovation. We are always looking at what’s coming next, devising products and services for the challenges of tomorrow.”

To learn more about AmTrust’s extended warranty solutions, visit https://amtrustfinancial.com/extended-warranties/specialty-risk.

![]()

This article was produced by the R&I Brand Studio, a unit of the advertising department of Risk & Insurance, in collaboration with AmTrust Financial. The editorial staff of Risk & Insurance had no role in its preparation.