Construction Risk

The Empire State Bind

The New York market for construction-related general liability risk is becoming smaller and ever more expensive, with legal costs increasing and carriers jumping ship. That makes risk management and safety more important than ever for property owners, general contractors and subcontractors wishing to secure meaningful general liability coverage in the state.

“Over the last 10 years, a lot of carriers got burned in New York,” since “some were willing to accept a submission from a prospect saying, ‘Yes, we’re doing all the things we need to with regards to risk transfer,’ with no follow up or confirmation,” said Adam Schnell, executive vice president with the casualty practice at WKFC Underwriting Managers, an MGA and a unit of Ryan Specialty in Melville, N.Y.

Those days are over. Today, said Schnell, “It’s a very tight market. I’d say there are maybe half a dozen surplus lines markets that are writing in the space and offering a viable GL product to property owners, general and trade contractors in New York.”

Legislative Quirks

To understand the problem fully, it’s important to know how construction workers tend to proceed when they’re injured — and to know a little something about New York labor laws.

Since construction workers employed by independent contractors cannot sue their employers directly, they’re initially likely to go through the workers’ compensation system for lost wages and medical expenses. But they don’t stop there.

“They’ll file a comp claim when they’re injured but they’ll frequently sue the property owner and the general contractor as well,” said Schnell.

In fact, this is how the system tends to work all across the country, said attorney Peter Gould, managing partner with Patton Boggs in Denver.

But New York is a different animal compared to other states, because for over a century, it has had certain laws on the books which greatly exacerbate the problem on the claims side.

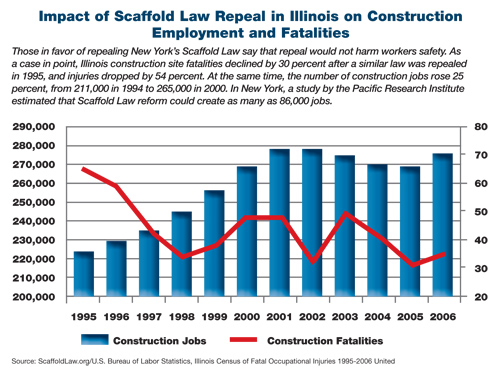

From an insurance industry perspective, one of the state’s most onerous provisions is the so-called “Scaffold Law.”

This law imposes “an absolute, non-delegable duty upon owners and general contractors to provide a safe working environment for laborers who work at elevation to protect them from ‘gravity-related’ accidents, such as such as falling from heights or being struck by an inadequately secured item,” said Schnell.

The law has been on the books since the late 1800s. It is an “absolute” liability doctrine in that, from Schnell’s perspective, “Even if workers were told 1,000 times to use a safety harness and flagrantly failed to protect themselves, property owners and general contractors cannot impose culpability on those injured.”

According to the Lawsuit Reform Alliance of New York, pure premium losses for construction projects in New York, especially New York City, are 300 percent higher than anywhere else in the nation, and these costs are a significant factor in every taxpayer-funded construction project — from roads and bridges to buildings and schools.

Don Baldini, assistant vice president and state affairs officer at Liberty Mutual in Boston said that in every state but New York, the legal concept of “comparative negligence” is often used in court to try and determine “what percent of the fault belongs to owners or general contractors.”

In New York, however, “You can’t even raise as a defense that a construction worker may have been grossly negligent and contributed to his own injury. The way that the workers’ compensation system and the general liability system tend to intersect in New York, in particular, leads to higher building costs, contributes to job losses, and is a burden for taxpayers,” he said.

Baldini says that Liberty Mutual continues to supply coverage in the state for contractors’ GL and workers’ compensation risks.

And yet it’s quite clear that as a result of the Scaffold Law and its sister statutes, the New York liability market definitely has a supply and demand problem, said Fred Heath, senior vice president with Marsh’s Construction Placement group in New York.

That’s why some of the key markets providing contractors’ general liability in New York, according to sources, are excess and surplus lines companies such as Princeton E&S Insurance Co., State National Cos., Catlin Group, Colony Specialty, Scottsdale Insurance Co. and American Empire Group.

Nevertheless, “you still have a small number of admitted carriers writing casualty risks in the New York marketplace,” Heath said. “These admitted markets will not entertain monoline general liability, however, and generally will require at least one other casualty line such as auto liability and/or workers’ compensation.”

But clearly, these remaining markets are very stringent in terms of how they underwrite the risk. The underwriting process will focus on loss control measures to eliminate fall hazards, detailed analyses of past claims experience and proper contractual risk transfer language for contractors that utilize subcontractors, said Heath.

Keys to Minimizing Risk

For his part, WKFC’s Schnell is able to offer clients a New York contractors program with a surplus lines carrier with an A+ rating from A.M. Best. He said that he is able to offer property owners and general contractors a guaranteed-cost primary GL, but noted that his program requires New York City subcontractors to carry $5 million, and $2 million for subcontractors outside of the five boroughs of the city.

Beside making sure the proper coverage and limits are in place, Schnell offered the following risk management recommendations for those hoping to secure meaningful coverage:

Beside making sure the proper coverage and limits are in place, Schnell offered the following risk management recommendations for those hoping to secure meaningful coverage:

• Have safety measures in place. For trade contractors, be sure to hire skilled and experienced workers and be sure to hold daily “toolbox” meetings with laborers to ensure that the proper equipment is being used and to enforce job site and public protection.

• Secure legal guidance. Seek coverage through an insurance program where legal guidance is available. Companies such as WKFC provide resources to buyers. It’s included in their price, and provided throughout their policy term. Insureds have access to legal consultation in order to navigate the complexity of exposures to ensure proper risk transfer.

• Don’t go cheap. “Some trade contractors may ‘cheap out’ and buy a $5,000 policy with a multitude of exclusions,” said Schnell.

A solid contractors’ GL program in New York State will have premiums ranging anywhere from 2 percent to 10 percent of the contractor’s per-project or annual gross revenue, he said.

Three or four years ago, prices maxed out closer to 4 percent of that, but things have changed.

“There had been a lot of capacity and carriers writing the business without realizing the risk they were taking,” Schnell said.

Gould, who specializes in environmental safety and health law, has some tips of his own for insurers.

He cautioned that, despite New York’s liberal labor laws, plaintiff’s attorneys will try to go for the jugular. In addition to showing a causal connection to the workers’ injury, they will almost certainly try to establish that the property owner or contractor being sued had a history of workplace accidents.

“They’ll want to show some kind of historical connection or indifference to employee well-being though a pattern of workplace safety problems,” the attorney said. “Insurers need to be careful when they agree to write policies for these property owners, contractors or subcontractors to understand the potential insured’s safety violation history. There has to be some higher level of due diligence involved to help mitigate or at least understand the risk.”

Because the risk of insuring a repeat safety violator is typically higher than insuring a company with a clean safety record, he said, insurers should also look at policyholders’ training documents to make sure they maintain rigorous training programs for their employees in such areas as fall protection, trenching and any other key construction project elements which tend to have higher workplace accident rates.

Gould said that companies with a wellness or fitness program in place at work may also represent better risks.

“Keeping people more healthy, nimble or flexible” can also mitigate the risk of serious injury, he said.

Insurers and insurance buyers should require that the subcontractors themselves have strict hiring practices in place where they “don’t just bring labor in off the street but hire qualified, competent people who’ve served a lot of time in their particular construction industry trade,” Gould said.

In addition, he said, it would be “a good idea to make this an insurance policy term.”

Gould also stressed the importance of requiring a zero-tolerance disciplinary policy for workplace safety infractions, where an employee caught working contrary to his or her safety training is terminated.

“This may be supplemented by carriers’ spot checks or audits of the insured’s workplace to ensure the insured takes safety matters at least as seriously as the carriers,” the attorney said.