The Driverless Future

Autonomous Risk

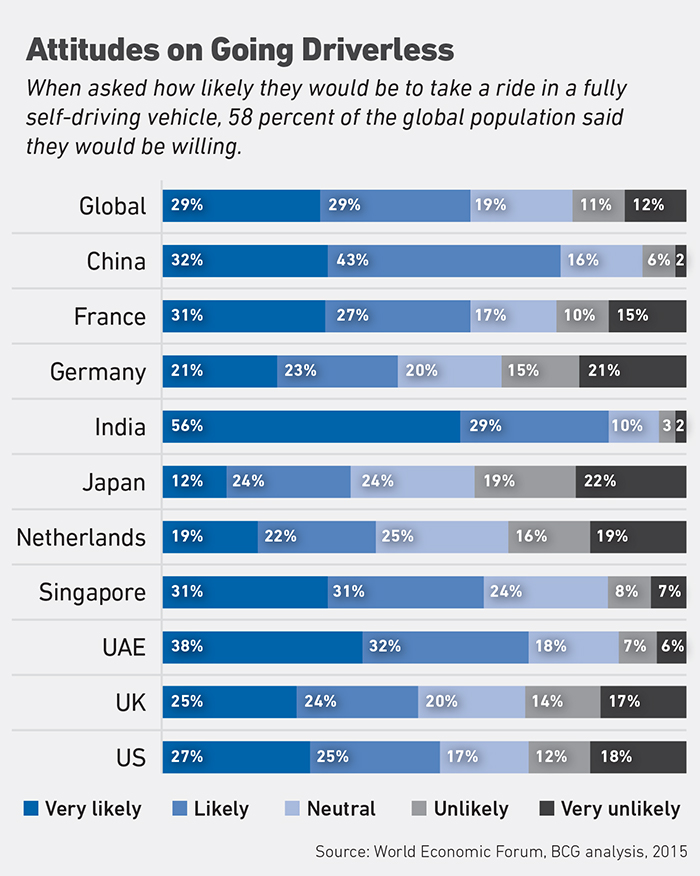

Outside of the rare Google car sighting, autonomous vehicles, or A.V.s, have mostly been the domain of futuristic action movies. That fictional future, though, is now.

A limited number of autonomous Volvo XC90s will be on the road this year. Audi’s self-driving A8 limousine is due out in 2017. Tesla plans to have fully autonomous vehicles available in 2018. Top executives at Ford and GM expect to launch fully autonomous vehicles by 2020. The U.S. Secretary of Transportation said at the 2015 Frankfurt Auto show that he expects driverless cars to be in use all over the world by 2025.

The twist, however, is that by 2025, the dominating force driving sales of those vehicles will most likely be commercial or public fleet operators, rather than private individuals.

VIDEO: Uber driverless takes to the streets in Pittsburgh.

While carmakers have been perfecting all this autonomous technology, the rest of the world was getting cozy with Zipcar, Car2Go, Uber and Lyft. Now those two disruptive concepts are merging, and the result is a seismic shift in the world as we know it.

Because driverless cars eliminate human error and human foibles like road rage and texting while driving, accident rates are expected to decline. Combined with an overall decrease in ownership, some say that will — eventually — cause a drastic upheaval in the auto insurance industry.

“Right now … everybody’s wringing their hands,” said John Lucker, global advanced analytics & modeling market leader with Deloitte Consulting.

John Lucker, global advanced analytics & modeling market leader, Deloitte Consulting

“Half of all premiums are going to disappear! The industry’s going to blow up! The personal lines market is going to disappear! And we’re saying, ‘Well, time out everybody.’ ”

The likely reality is more nuanced. Deer will still dart into the road in the blink of an eye. Stray softballs and golf balls will still take out windshields. Car theft isn’t going away. And of course, machines can malfunction or be hacked. Insurance will remain as necessary as ever, but coverage needs will shift in a variety of ways.

“There’s going to be a blurring of the distinctions between various types of commercial insurance and personal insurance,” said James Guszcza, U.S. chief data scientist for Deloitte Consulting.

Sorting through it all is going to be incredibly complicated for carriers, as personal ownership slowly gives way to increased commercial ownership, in the form of driverless “Uber armies” or large A.V. fleets. There will also be a long period when non-autonomous, semi-autonomous, and fully autonomous vehicles will all be in the mix to varying degrees.

“Until all of the vehicles on the road are autonomous, how do you mix and match this?” asked Lucker.

“Your car is acting on its own, then it crashes into somebody who’s driving. How do you figure out who’s at fault? And then, is it a software issue? Is it your liability because you [own the car]? Was it the fault of the [human driver]?

“I don’t think that these things are going to go away,” Lucker said. “There’s obviously a blending of commercial auto, personal auto, potentially E&O for software developers, potentially some sort of product liability risk if a sensor didn’t work properly on the autonomous vehicle … there’s a lot of stuff going on here that traditionally has always been assumed to be a simple personal auto coverage.”

“This is a spectrum,” said Guszcza, “and we’re moving along that spectrum.”

How Quick a Shift?

Opinions vary widely on how fast this transformation will come to pass. Looking out to 2025, “you are going to find universally available cheap automotives, but those are probably going to be bought by self-drive fleet-manager-as-a-service type companies,” said Chris Smedley, CEO of Digital Habitats Corp. and longtime technology entrepreneur.

“Most of us are going to pay for transportation on a per-use basis.”

The rise of mobility as a service (MaaS) is taking hold quickly, and human drivers are indeed being pushed out. Uber CEO Travis Kalanick expects the entire Uber fleet to be driverless by 2030. The foundation is already being laid.

“I can’t imagine how many years it’s going to take for there to be mechanisms where police or road construction can be updated in real time to the point where true autonomous vehicles can navigate.” —John Lucker, global advanced analytics & modeling market leader, Deloitte Consulting

In August, the MIT-born company NuTonomy launched a test fleet of six self-driving taxis in a small section of Singapore, with human drivers on board to take over if necessary. Uber and Volvo also announced plans to launch a fleet of 100 self-driving Uber vehicles in Pittsburgh by the end of summer. The goal is to eliminate human drivers altogether — eventually. Once that happens, Uber’s Kalanick said, its service will be so inexpensive and broadly available as to make personal car ownership obsolete.

Researchers seem to agree. A 2015 Barclay’s report concluded that auto sales will dip by as much as 40 percent within the next 25 years, as traditional ownership gives way to family autonomous vehicles, shared autonomous vehicles, and autonomous vehicle pooling (think Waze Carpool with no drivers). Barclays estimated that one shared, pooled vehicle could do the work now accomplished by 17 vehicles.

But there’s a silver lining for car manufacturers. A January 2016 McKinsey report suggested that the decline in private vehicle sales will be offset by increased sales of commercially and publicly owned shared fleet vehicles. Those vehicles will need to be replaced far more often due to heavy usage. The report concluded that overall global car sales would drop from the current annual growth rate of 3.6 percent to 2 percent by 2030.

The bottom line is that until somebody figures out how to make Star Trek’s transporter beam a reality, cars and trucks will still be the lifeblood of commerce and society. It’s the way we use them that’s about to shift in a variety of ways, and every manner of industry will need to assess how the shift will affect them.

Like falling dominoes setting off chain reactions, the mobility revolution will strike blows across multiple industry sectors.

Impact Across Industries

The beleaguered petroleum industry is in for more pain, because a steadily growing percentage of new autonomous cars will be electric. The taxi industry, already ailing, appears to be doomed.

James Guszcza, U.S. chief data scientist, Deloitte Consulting

The parking industry will take heavy hits — who needs a parking space when you Uber to work? Even those who do choose to buy their own autonomous cars won’t need to park — they can just send their cars home to wait.

Prevailing wisdom says that accidents will decline sharply as A.V. usage increases, which could send the $62 billion repair industry into a tailspin. Automotive computer repair will move to the fore as collision repair needs shrink.

Car-sharing and ride-hailing services, now the disruptors, will become the disrupted unless they evolve as Uber is already trying to do. The traditional car rental industry will also be forced to adapt or die.

The same changes will drive a new dynamic in public transportation as well. In fact, it’s already begun.

In April, the City of Beverly Hills, Calif., unanimously passed a resolution to develop a public transportation system consisting of driverless municipal shuttles. The idea is spreading. All seven finalists in the U.S. Department of Transportation’s 2016 Smart City Challenge submitted proposals that included semi- or fully autonomous vehicles.

Columbus, Ohio, winner of the $50 million challenge, plans a fleet of connected, electric, autonomous shuttles to ferry people around its business district. Other cities’ proposals included plans to shuttle people between transit hubs and airports autonomously, or to have self-driving vehicles handle deliveries and municipal transportation of materials.

For the average business, this shifting dynamic will be a mixed bag. Eliminating drivers will obviously have a significant impact on the cost of transporting or delivering products. However, as new players enter the autonomous on-demand fleet space, trying to grab for market share, choices for business leaders could become cloudy.

“There’s going to be a blurring of the distinctions between various types of commercial insurance and personal insurance.” — James Guszcza, U.S. chief data scientist, Deloitte Consulting

How do you properly vet your vendor? How much do you know about their parts and programming and how safe or reliable their driverless units are? It remains to be seen whether a company could be held responsible if a fleet vendor’s car were to cause life or property damage while delivering its products.

It will likely take decades of litigation to achieve any clarity on these types of liability issues.

Deep, Deep Data

The upside for both insurers and insureds is that the newest automotive technologies — and the data they collect — will create transparencies to a degree barely ever imagined before.

The new wave of vehicles will be equipped with ever-more-sophisticated sensors and telematics, enabling an unprecedented degree of precision in adjusting as well as pricing, said Lou Brothers, senior manager, West Monroe Partners.

In the event of a crash, adjusters will simply download both vehicles’ “black box” data and know instantly what happened and why, improving accuracy and eliminating the need for investigations.

“The device knows,” said Brothers.

Lou Brothers, senior manager, West Monroe Partners

“It knows what it did, it knows what the other driver did, it knows what you did. And if the other car’s a smart car, we know all the components … the friction on the road, the speed, the position of the gas pedal and brake pedal, deceleration patterns … now there’s no question about who’s at fault.”

On-board technology will give underwriters access to more varied and deeper layers of data, potentially enabling them to fine-tune premiums specific to actual usage, said Brothers.

“Lou’s driving on I-78 heading west out of New York through the Holland Tunnel. Say we know that on the entry point on the Holland Tunnel, he has a 2 percent greater chance of a side-by-side collision because of the funneling that happens there. Therefore for that period of time, instead of paying $3.00 for insurance he’s going to pay $3.50 for insurance — just for that 10 minute period.

“We know everything about the car, where it is, how long it’s there for, we know the accident statistics of all of those different areas — you could really drive yourself into a very detailed, nuanced view of this one driver, in this one car, in this one scenario, at this moment.”

Admittedly, said Brothers, that capability is still a long way off. “The amount of computation, the amount of analysis and of thought that would have to be put into those risk models would be insane,” he said.

“We’re talking about … driving down to the statistic of one.”

But when it happens, it presents some very attractive possibilities for the businesses that will be entrusting their products to autonomous on-demand fleets.

If allowed access to the data collected from commercial fleets, companies would be able to make better decisions about the risk level of each provider, and even about the routes traveled by vehicles being used to conduct their business.

It could also drive a conversion to usage-based automotive insurance, giving commercial fleet owners more power to control their premiums and offer more competitive rates to customers.

Imagine a carrier sending a message that said, maybe you should consider these alternate routes because they’re safer. Or maybe suggesting taking a longer route because it’s better paved or lowers the overall risk of the route.

In the end, money talks, said Brothers. If your carrier told you that if you were to leave 10 minutes earlier every day, your premiums would go down $80, chances are good that you’d leave 10 minutes earlier.

“That kind of real-time alert could be a very positive thing that I think people would welcome.”

Infrastructure Lacking

Risk managers trying to map out how the mobility shift will impact their organizations still have some time to get a handle on it. Despite the current race to put autonomous vehicles on the road, some believe the pace of change will be slow because the infrastructure to support a driverless world doesn’t exist, and few are talking about how to create it.

That’s why projects like NuTonomy’s Singapore test and the Uber/Volvo Pittsburgh venture make sense, because they’re constrained to areas that can be mapped precisely.

The trickier problem is that even keeping vehicles to proscribed routes won’t eliminate unknowns, experts said.

“Let’s say a sinkhole gets formed because of a massive rainstorm,” said Lucker. “How are the police going to alert this global GPS repository that Maple Street is now closed, so every single car knows not to turn down Maple Street?

“Worse, what if there’s an obstacle or accident halfway down a road, the cars don’t know that, and a whole string of cars goes down the road and they form a traffic jam. How will the cars sort out how to get out of there?

“There is no mechanism to create the global GPS database repository of changing road conditions and changing obstacles that an autonomous car is going to have to have access to in real time in order for something to be truly autonomous,” Lucker said.

“I can’t imagine how many years it’s going to take for there to be mechanisms where police or road construction can be updated in real time to the point where true autonomous vehicles can navigate.” &