Robotics in the Workplace

Helping Hands?

It’s probably way too soon to start dreaming up insurance products that will respond to the risk that robots are going to rise up and annihilate humankind. And good luck finding the market capacity for it anyway.

However, robots and robotics are fast becoming a fixture of our reality, and the industry is poised for rapid expansion.

Robots, in some form or another, have been present in the manufacturing sector since 1962, when a New Jersey General Motors factory began using a robot to do spot welding and extract die castings. By the ’70s, increasingly sophisticated machines, operated by minicomputers, were being widely used for small parts assembly.

Robotics have long since moved away from the assembly line. Robots are present everywhere from warehouses to hospitals, from farms to laboratories, and from the military to mines and more.

One of the latest robotic forays into the workplace is at the Aloft hotel in Cupertino, Calif., where “The Botlr” — a service robot that looks like a distant cousin of R2-D2 — is being used to make small deliveries to guests’ rooms. Robots may soon be flipping your burgers or picking the grapes that make your favorite wine.

Video: The Botlr, a robotic bellhop built for Aloft Hotels, delivers an item to a guest in his room.

But the application of robotics is going ever deeper.

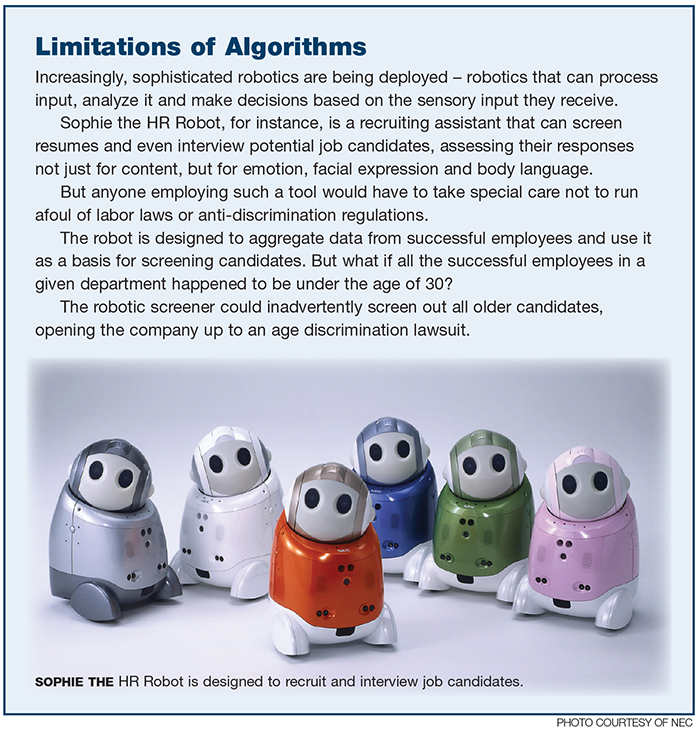

The development of robots connected to the Internet, big data, the cloud and advanced computing technology such as artificial intelligence (AI) algorithms are bringing a new class of robots into the workplace — those that can sense, think and act based on specific data and sensory input, and make routine decisions.

In June, the Associated Press began experimenting with having machines write short business stories. The news organization said that eventually, the majority of its U.S. corporate earnings stories would be produced using automation. (As of press time, Risk & Insurance® is not yet employing robotic journalists.)

There are obvious positives to the growth of robotics in the workplace. It makes sense to give robots the high-turnover jobs that are mind-numbingly rote, as well as those jobs and tasks considered extremely dangerous.

But the change that is coming may be far more profound. Garry Mathiason, co-chair of the Robotics, Artificial Intelligence and Automation practice group at Littler Mendelson in San Francisco, cited a 2013 study published by the Oxford Martin School, examining automation potential across the U.S. labor market.

According to the study, said Mathiason, “47 percent of jobs currently done by people in the United States will be done by machines and software within one to two decades. That doesn’t mean there’s going to be 50 percent unemployment; it does mean there’s going to be that much change taking place.”

(For the record, the Oxford Martin study said that insurance underwriters are in the highest risk category for being taken over by automation, just ahead of claims and policy processing personnel, claims adjusters, examiners and investigators.)

“2010 was a turning point in terms of the acceleration of the technology and its implications,” said Mathiason. “There is a change taking place that will be the equivalent of the Internet in terms of what it will do to the workplace.”

Video: At the fulfillment center of North Reading, Mass.-based Kiva Systems, 100 robots work alongside 300 fulfillment associates.

Pointing Fingers

So far though, companies that employ robots see the importance of having human checks and balances on the robots’ work. Many companies are actually increasing staffing levels to support their robotic equipment.

That raises concerns about whether employees are at increased risk of harm by robotic equipment, or may inadvertently interfere with safe robotic operations. A fair number of workplace fatalities related to robotics have occurred in the last decade or two.

As it stands, employers are covered by existing workers’ comp statutes if a robot were to cause a workplace injury or fatality, the same as they would be in the event of an injury or death caused by any other piece of equipment.

The same would not be true, however, if a robot were to injure a customer, a vendor or any other visitor to a facility. In those cases, who can expect to face a lawsuit? The answer, for now, is: It depends.

Liability issues get sketchy when you factor in the element of closed versus open robotics.

In a closed robotics system, a robot is designed and manufactured for one specific purpose. (iRobot’s Roomba, for instance, is a vacuum — period — no matter how many YouTubers use it as an amusement park ride for their cats.)

But with an open robotic system, independent developers would be able to create programs, or apps, to allow the system to accomplish different user-defined tasks, adding more potential culprits in the event of a claim.

“This is going to be a big issue,” said Stephen Wu, an attorney who is of counsel to Silicon Valley Law Group based in San Jose, Calif.

“[In the event of a robot-related accident], I’m going to be doing an investigation and using experts to determine the root cause. Was it my own environment? Was it the hardware manufacturer? Was it the firmware manufacturer? Was it the application software? Was it the operating system manufacturer? Or was it some subcomponents thereof? Or else … was it a data service provider [such as one providing mapping data]?”

These questions will grow still more complicated with the growth of adaptive technology — meaning when robots make decisions on their own based on the data and sensory input they receive.

“Increasingly, adaptive intelligence is being built in where the robot is going to be changing what it does based on external stimuli,” said Drew Haaser, U.S. technology practice leader for Marsh.

“Let’s say it’s putting welds on an auto and it’s been programmed to sense the properties of the materials it’s welding and adapt … . If it makes the wrong decision — what are going to be the legal implications to that?”

That question reaches a whole other level when the consequence is a loss of life.

“What if you have a robot that is … facing the decision to either run over your daughter or hit a school bus full of kids, what is the right thing to do in that situation?” asked David Beyer, managing member of Digital Risk Resources.

“I think that it’s a very complex issue. … They try to think through a lot of these situational risks but you can’t predict all the risks all the time.”

“I think what we’re going to see is that all parties are going to be drawn into these lawsuits. They’re all going to have their feet put to the fire and they’re all going to point at each other. Unfortunately, a jury is going to have to decide these things.” — David Beyer, managing member, Digital Risk Resources

It’s crucial, said Guy Fraker, that we remember robotics is not synonymous with infallible.

“You can say, ‘We can fix that with an algorithm.’ But can you program for that kind of variability in advance? No,” said Fraker, former director of business trends and foresight for State Farm and co-founder and CEO of consultancy Autonomous Stuff.

“We’re learning new things about the technology every day.”

“These are not dumb devices anymore,” said Haaser, “and when they make mistakes in how they interpret stimuli, is it a professional liability error in the design of the product or in the software as opposed to a straightforward bodily injury/property damage claim?”

As more businesses incorporate adaptive technology into the workplace and robotics follow cues based on what they’re learning in their environments, the more that risk management will be expected to have thought through all of the implications of how the robot or robotic systems might respond.

Eventually, there will be cases where robots make “correct” decisions that result in tragic outcomes.

Several experts cited the example of a driverless car faced with a choice of hitting a tractor trailer or hitting an occupied baby stroller. Most assume that the car would attempt to minimize damage by hitting the stroller.

In a case like that, “Was it a mistake? Well, no,” said Haaser.

“Was it what a human with a duty to care would have done? No! And how will the courts treat that? Unfortunately, there are a whole lot of questions and not a whole lot of answers yet as to how the courts will treat that.”

“I think what we’re going to see,” said Beyer, “is that all parties are going to be drawn into these lawsuits.

“They’re all going to have their feet put to the fire and they’re all going to point at each other. Unfortunately, a jury is going to have to decide these things.”

Human Augmentation

The extremely good robotics news is that a great many of the developments coming out of the industry have the potential to decrease employer exposure rather than increase it.

In particular, advances in exoskeleton technology are moving to the forefront, even gaining a global stage during the 2014 World Cup, when a young paraplegic man made the first official kick of the event, wearing a mind-controlled robotic exoskeleton.

Video: Juliano Pinto, 29-year-old paraplegic man, successfully made the first kick of the 2014 World Cup in Sao Paulo, wearing a full body robotic suit.

In South Korea last year, employees of Daewoo Shipbuilding and Marine Engineering helped test a prototype of a full-body exoskeleton that will enable them to lift large hunks of metal, pipes and other objects without excess exertion or risk of strain or injury.

“In basic safety and loss control, the first line of defense is to engineer the risk out; robotics is one of the purest forms of ‘engineering out’ a risk,” said Bill Spiers, vice president and risk consulting manager, Lockton Cos.

Bill Spiers, vice president and risk consulting manager, Lockton Cos.

“You have eliminated the human interaction around a task that’s going to create soft tissue strains that are very costly.”

Industry leaders such as Ekso Bionics and Cyberdyne are actively producing exoskeletons that have a broad range of applications. Robotic suits could dramatically reduce injury risk for workers with physically intensive jobs, potentially enhancing productivity at the same time.

“Wearable technology has the potential for ameliorating some [health and safety] concerns,” said Littler Mendelson’s Mathiason. “You can see it someday becoming as common as safety shoes.”

Mathiason said this may eventually be of equal importance as applied to Americans with Disabilities Act accommodation issues.

“You have people who couldn’t perform the essential functions of the job. Then seven million paraplegics can suddenly walk and do things nobody thought they would ever do again,” he said.

For workers who’ve already suffered temporary or permanent disabling injuries, exoskeletons could eventually open the doors for new means to keep injured workers on the job. Even severely disabled employees could potentially be returned to productive and essential work, increasing quality of life for injured workers while saving employers millions in partial and total disability payments.

“You have people who couldn’t perform the essential functions of the job. Then seven million paraplegics can suddenly walk and do things nobody thought they would ever do again.” — Garry Mathiason, co-chair of the Robotics, Artificial Intelligence and Automation practice group, Littler Mendelson

Currently, 330 of Cyberdyne’s HAL-5 full-body exoskeletons have been leased to hospitals across Japan, where they assist patients with muscle weakness or disabilities due to stroke and spinal cord injuries. In some industries, this area of robotics could virtually eliminate obstacles to accommodating injured or disabled workers.

Due Diligence

As companies make critical decisions about incorporating robotics into their operations, it’s important to bring risk management into the loop early on.

While companies increasingly transition processes to robotics for the sake of cost savings, said Haaser, “the challenge for the risk manager will be to see that some of those savings are being reinvested back into risk management.”

But the most urgent piece is getting risk management involved in decisions about capital expenditures like robotics from the get-go.

John Abbott, an account executive at Arthur J. Gallagher & Co., said there are a host of questions that risk managers need to think through in advance.

“Are you going to be using it to do something that’s never been done before? Do you want to go into an area where there’s a potential environmental issue that may impair the robot’s performance? Robots are mechanical and electrical systems — any robotic system is prone to wear and tear and failure to some degree.”

Wu of the Silicon Valley Law Group added that due diligence is of utmost importance when selecting vendors for robotic system components, including whether there are any kinds of certifications that apply to the machines.

“Is there a UL-type seal of approval that we could look for that can be had?” Wu asked. “And what kind of testing went into the robots in the first place?”

Issues such as hackers and the potential for fraud must also be given consideration, said Fraker. “For every great capability that’s ever been developed … there’s an opposing potential dark side,” he cautioned.