Specialty Brokers

Pros and Cons of Specialty Consolidation

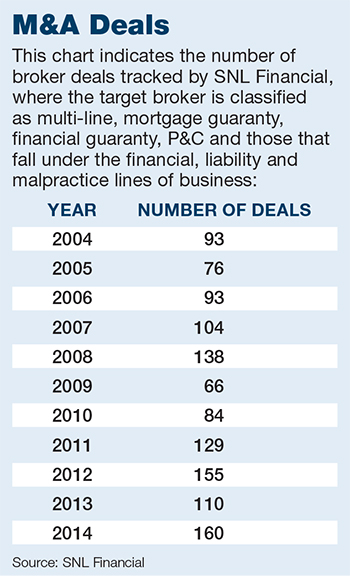

Merger and acquisition activity is rife in the insurance space and in the specialty brokering market in particular. According to M&A advisory firm MarshBerry, there were 220 acquisitions in the U.S. broker sector in 2014, and 49 of them involved wholesale brokers and managing general agents and underwriters (MGAs and MGUs).

“Making this surprising is that specialty distributors are significantly outnumbered by retail insurance agencies,” the firm said, noting that there are approximately 1,250 specialty distributors in the U.S. compared to 25,000 retail agencies. In other words, specialty M&A accounted for 22 percent of all broker M&As despite specialty players being outnumbered 20 to 1.

According to Julie Herman, associate director of financial services ratings at Standard & Poor’s, consolidation in the specialty brokering space mirrors M&A activity among insurers, many of whom have been buying specialty teams as a way of managing their underwriting cycle in a low rate environment.

Julie Herman

Associate Director of

Financial Services Ratings,

Standard & Poor’s

“Brokers follow the trends of insurers, so it makes sense they would follow them into specialty,” she said.

“Cheap debt, low interest rates and private equity capital entering the space, combined with competition driving up multiples, makes a plentiful M&A environment. And there are so many opportunities out there, especially in the U.S. broker markets — there are thousands of brokers and the market is very fragmented.”

Herman added that insurers are increasingly focusing on streamlining the number of distribution partners they do business with, exacerbating the broker consolidation trend.

“It is becoming harder for small brokers to compete against bigger players in a softening market in which there is a need to be more sophisticated. Most small players don’t have the resources to invest in big data and technology, so it often makes sense to sell,” she said.

“The losers are the specialty wholesalers who don’t want to sell but might not to be able to adapt to the marketplace and get left behind.”

RIMS board director Gordon Adams is chief risk officer for Tri-Marine International, a fishing company with specialty marine risks. He said he’s seen little evidence of contraction in the marine broking space, but in other areas such as credit insurance there are very few specialist brokers and there is consolidation.

“That is a concern as there are less competitors and therefore we have less ability to do an RFP. Insurance is a personal relationships industry. Companies may miss out on developing personal relationships with boutique brokers in favor of using the big brokers. The larger brokers try to be all things to all people, and that’s certainly not always successful.”

In September 2014, JLT — the world’s largest specialty brokerage — began a concerted push into the U.S. According to Doug Turk, chief marketing officer for JLT Specialty in the U.S., the broker may consider joining the M&A party.

“We’re very open and interested in seeing what’s out there, but we are going to be very selective to make sure any acquisition target fits within our specialty strategy and also with the culture of JLT,” he said.

Impact on Clients

However, Turk challenged the view that broker consolidation leads to less choice for the client. Large clients have had limited choice for some time, he said, while JLT’s move into the U.S. as a retail specialty broker has helped meet demand for more choice when it comes to specialty risk.

“[Consolidation] doesn’t change the markets we go to or the solutions we offer. Underwriting consolidation is something we have to deal with, but with most consolidations, teams remain largely intact. It’s a good time for clients because they can get more out of their relationships with brokers,” he said.

There is no doubt that if a small broker is bought out by a more sophisticated buyer, its clients should benefit from an array of value-adding services.

“There are always two sides to every coin but right now the positives outweigh the negatives for the insurance buyer, if successful operational and financial execution is in place,” said Herman.

Scott Burton, a partner with Sutherland, Asbill & Brennan in Atlanta, agreed.

“Ultimately, the effects of consolidation on resulting scale and the continued gains in efficiency and expertise should result in better rates and terms for many clients,” he said.

Larger brokers absorb the specialist expertise of small wholesalers but can then use their superior infrastructure to scale up these operations, bringing specialty capability to a wider audience. The key is of course to ensure the acquired teams are not dismantled, diluted or commoditized by the merger.

Specialist Focus

Companies that don’t sell up must capitalize on their ability to offer bespoke service.

“Smaller brokers can compete by differentiating and having a product,” said Herman.

“If they are able to maintain key relationships and use their niche expertise to design specialty programs, carriers will still want to do business with them.”

Turk agreed that while many of the largest brokers look at business in terms of yield and commodification, specialists use their industry expertise to create unique and innovative products for their chosen client bases. This is, he said, what makes specialty-focused JLT different than the likes of Marsh, Aon and Willis.

“There is an increasing role for true specialty brokers who have industry knowledge — an ability to understand business first and risk second, and the ability to translate that understanding into customized solutions,” he said.

Tri-Marine’s Adams is a strong believer in the value of working with the most specialized brokers out there.

“Having a department that is able to service a specialty area is not the same as specializing in a specialty area,” he said, contending that boutique brokers are more likely to have a closer relationship with the client and offer dedicated, individualized service than broad-brush broking houses.

“We want our broker to have expertise and a predilection to our areas of business. The broker we selected at our last RFP said ‘we are heavily focused on marine, and because of that we don’t offer the same abilities in property/casualty or workers’ compensation, so we’d like to partner with a very strong regional broker who can provide these areas.’ That’s the direction we went in, and together they provide what we need.”

For many companies, choosing a one-stop-shop broker may be equally, if not more appealing than using a patchwork of specialists. One area the large buyers have a clear advantage over their smaller target firms is in their ability to service a rapidly internationalizing corporate sector.

“Globalization is fundamentally changing the expectations of our clients. International clients today demand seamless global coverage,” said Turk. “There’s a growing requirement to comply with local regulations in international locations. The world is becoming so much more complex, and companies demand that the brokers they work with have the knowledge to make sure they are in compliance with local regulations when placing policies.

“I’ve been in the industry 44 years and I’ve seen expansion and contraction a number of times during my career.” — Doug Turk, chief marketing officer, JLT Specialty in the U.S.

“Smaller brokers don’t have a global umbrella capability. The problem for them is that virtually all large clients now require it. Even if you are a very niche specialty broker you have got to have that global capability,” he added.

Adams said that as long as a broker can access major insurance markets, the carriers can take care of the global program.

“We have offices across the globe, and buy insurance on a global basis through our corporate risk management program. What is important is to have a global insurance carrier that can address those needs, and a broker that can access the resources of that carrier,” he said.

“I don’t find it limiting to use a specialty broker with only two or three offices because they deal with the likes of Lloyd’s, ACE and AIG, who have boots on the ground all around the world. One call to the local broker means we can access those boots on the ground pretty much any place we have a need.”

Global brokers are, however, more likely to be able to access increasingly popular alternative risk transfer channels such as insurance-linked securities (ILS), as well as being able to offer far superior analytics than small independents.

According to Turk, “data analysis and insight is increasingly driving how insurance is procured and how companies assess their risk.”

Adams, however, said that there are still pockets of industry for which data is not yet a necessity.

He also said that while consolidation is rife among specialty brokers right now, it’s nothing new.

“I’ve been in the industry 44 years and I’ve seen expansion and contraction a number of times during my career. Every time there is a consolidation and the big brokers gobble up the specialty brokers, it’s not long before you see people peeling off and starting again, and the cycle starts over.”

For now, according to Herman, specialty M&A is set to continue.

“All the ingredients that made for an active M&A market in 2014 are still there and I don’t see why it would slow,” she said.

“The opportunities are still there and there are so many brokers that are ripe for being acquired.”

This could mean less choice for insurance buyers in an increasingly commoditized market. For those whose glasses are half full, the trend may mean specialty expertise is available to a wider audience.