Insurtech

Kiss Your Annual Renewal Goodbye; On-Demand Insurance Challenges the Traditional Policy

The gig economy is growing. Nearly six million Americans, or 3.8 percent of the U.S. workforce, now have “contingent” work arrangements, with a further 10.6 million in categories such as independent contractors, on-call workers or temporary help agency staff and for-contract firms, often with well-known names such as Uber, Lyft and Airbnb.

Scott Walchek, founding chairman and CEO, Trōv

The number of Americans owning a drone is also increasing — one recent survey suggested as much as one in 12 of the population — sparking vigorous debate on how regulation should apply to where and when the devices operate.

Add to this other 21st century societal changes, such as consumers’ appetite for other electronic gadgets and the advent of autonomous vehicles. It’s clear that the cover offered by the annually renewable traditional insurance policy is often not fit for purpose. Helped by the sophistication of insurance technology, the response has been an expanding range of ‘on-demand’ covers.

The term ‘on-demand’ is open to various interpretations. For Scott Walchek, founding chairman and CEO of pioneering on-demand insurance platform Trōv, it’s about “giving people agency over the items they own and enabling them to turn on insurance cover whenever they want for whatever they want — often for just a single item.”

“On-demand represents a whole new behavior and attitude towards insurance, which for years has very much been a case of ‘get it and forget it,’ ” said Walchek.

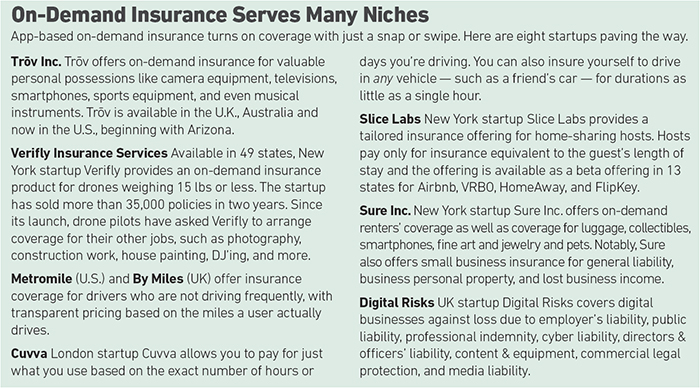

Trōv’s mobile app enables users to insure just a single item, such as a laptop, whenever they wish and to also select the period of cover required. When ready to buy insurance, they then snap a picture of the sales receipt or product code of the item they want covered.

Welcoming Trōv: A New On-Demand Arrival

While Walchek, who set up Trōv in 2012, stressed it’s a technology company and not an insurance company, it has attracted industry giants such as AXA and Munich Re as partners. Trōv began the U.S. roll-out of its on-demand personal property products this summer by launching in Arizona, having already established itself in Australia and the United Kingdom.

“Australia and the UK were great testing grounds, thanks to their single regulatory authorities,” said Walchek. “Trōv is already approved in 45 states, and we expect to complete the process in all by November.

“On-demand products have a particular appeal to millennials who love the idea of having control via their smart devices and have embraced the concept of an unbundling of experiences: 75 percent of our users are in the 18 to 35 age group.” – Scott Walchek, founding chairman and CEO, Trōv

“On-demand products have a particular appeal to millennials who love the idea of having control via their smart devices and have embraced the concept of an unbundling of experiences: 75 percent of our users are in the 18 to 35 age group,” he added.

“But a mass of tectonic societal shifts is also impacting older generations — on-demand cover fits the new ways in which they work, particularly the ‘untethered’ who aren’t always in the same workplace or using the same device. So we see on-demand going into societal lifestyle changes.”

Wooing Baby Boomers

In addition to its backing for Trōv, across the Atlantic, AXA has partnered with Insurtech start-up By Miles, launching a pay-as-you-go car insurance policy in the UK. The product is promoted as low-cost car insurance for drivers who travel no more than 140 miles per week, or 7,000 miles annually.

“Due to the growing need for these products, companies such as Marmalade — cover for learner drivers — and Cuvva — cover for part-time drivers — have also increased in popularity, and we expect to see more enter the market in the near future,” said AXA UK’s head of telematics, Katy Simpson.

Simpson confirmed that the new products’ initial appeal is to younger motorists, who are more regular users of new technology, while older drivers are warier about sharing too much personal information. However, she expects this to change as on-demand products become more prevalent.

“Looking at mileage-based insurance, such as By Miles specifically, it’s actually older generations who are most likely to save money, as the use of their vehicles tends to decline. Our job is therefore to not only create more customer-centric products but also highlight their benefits to everyone.”

Another Insurtech ready to partner with long-established names is New York-based Slice Labs, which in the UK is working with Legal & General to enter the homeshare insurance market, recently announcing that XL Catlin will use its insurance cloud services platform to create the world’s first on-demand cyber insurance solution.

Another Insurtech ready to partner with long-established names is New York-based Slice Labs, which in the UK is working with Legal & General to enter the homeshare insurance market, recently announcing that XL Catlin will use its insurance cloud services platform to create the world’s first on-demand cyber insurance solution.

“For our cyber product, we were looking for a partner on the fintech side, which dovetailed perfectly with what Slice was trying to do,” said John Coletti, head of XL Catlin’s cyber insurance team.

“The premise of selling cyber insurance to small businesses needs a platform such as that provided by Slice — we can get to customers in a discrete, seamless manner, and the partnership offers potential to open up other products.”

Slice Labs’ CEO Tim Attia added: “You can roll up on-demand cover in many different areas, ranging from contract workers to vacation rentals.

“The next leap forward will be provided by the new economy, which will create a range of new risks for on-demand insurance to respond to. McKinsey forecasts that by 2025, ecosystems will account for 30 percent of global premium revenue.

“When you’re a start-up, you can innovate and question long-held assumptions, but you don’t have the scale that an insurer can provide,” said Attia. “Our platform works well in getting new products out to the market and is scalable.”

Slice Labs is now reviewing the emerging markets, which aren’t hampered by “old, outdated infrastructures,” and plans to test the water via a hackathon in southeast Asia.

Collaboration Vs Competition

Insurtech-insurer collaborations suggest that the industry noted the banking sector’s experience, which names the tech disruptors before deciding partnerships, made greater sense commercially.

“It’s an interesting correlation,” said Slice’s managing director for marketing, Emily Kosick.

“I believe the trend worth calling out is that the window for insurers to innovate is much shorter, thanks to the banking sector’s efforts to offer omni-channel banking, incorporating mobile devices and, more recently, intelligent assistants like Alexa for personal banking.

“Banks have bought into the value of these technology partnerships but had the benefit of consumer expectations changing slowly with them. This compares to insurers who are in an ever-increasing on-demand world where the risk is high for laggards to be left behind.”

As with fintechs in banking, Insurtechs initially focused on the retail segment, with 75 percent of business in personal lines and the remainder in the commercial segment.

“Banks have bought into the value of these technology partnerships but had the benefit of consumer expectations changing slowly with them. This compares to insurers who are in an ever-increasing on-demand world where the risk is high for laggards to be left behind.” — Emily Kosick, managing director, marketing, Slice

Those proportions may be set to change, with innovations such as digital commercial insurance brokerage Embroker’s recent launch of the first digital D&O liability insurance policy, designed for venture capital-backed tech start-ups and reinsured by Munich Re.

Embroker said coverage that formerly took weeks to obtain is now available instantly.

“We focus on three main issues in developing new digital business — what is the customer’s pain point, what is the expense ratio and does it lend itself to algorithmic underwriting?” said CEO Matt Miller. “Workers’ compensation is another obvious class of insurance that can benefit from this approach.”

Jason Griswold, co-founder and chief operating officer of Insurtech REIN, highlighted further opportunities: “I’d add a third category to personal and business lines and that’s business-to-business-to-consumer. It’s there we see the biggest opportunities for partnering with major ecosystems generating large numbers of insureds and also big volumes of data.”

For now, insurers are accommodating Insurtech disruption. Will that change?

“Insurtechs have focused on products that regulators can understand easily and for which there is clear existing legislation, with consumer protection and insurer solvency the two issues of paramount importance,” noted Shawn Hanson, litigation partner at law firm Akin Gump.

“In time, we could see the disruptors partner with reinsurers rather than primary carriers. Another possibility is the likes of Amazon, Alphabet, Facebook and Apple, with their massive balance sheets, deciding to link up with a reinsurer,” he said.

“You can imagine one of them finding a good Insurtech and buying it, much as Amazon’s purchase of Whole Foods gave it entry into the retail sector.” &