Risk Focus: Asia

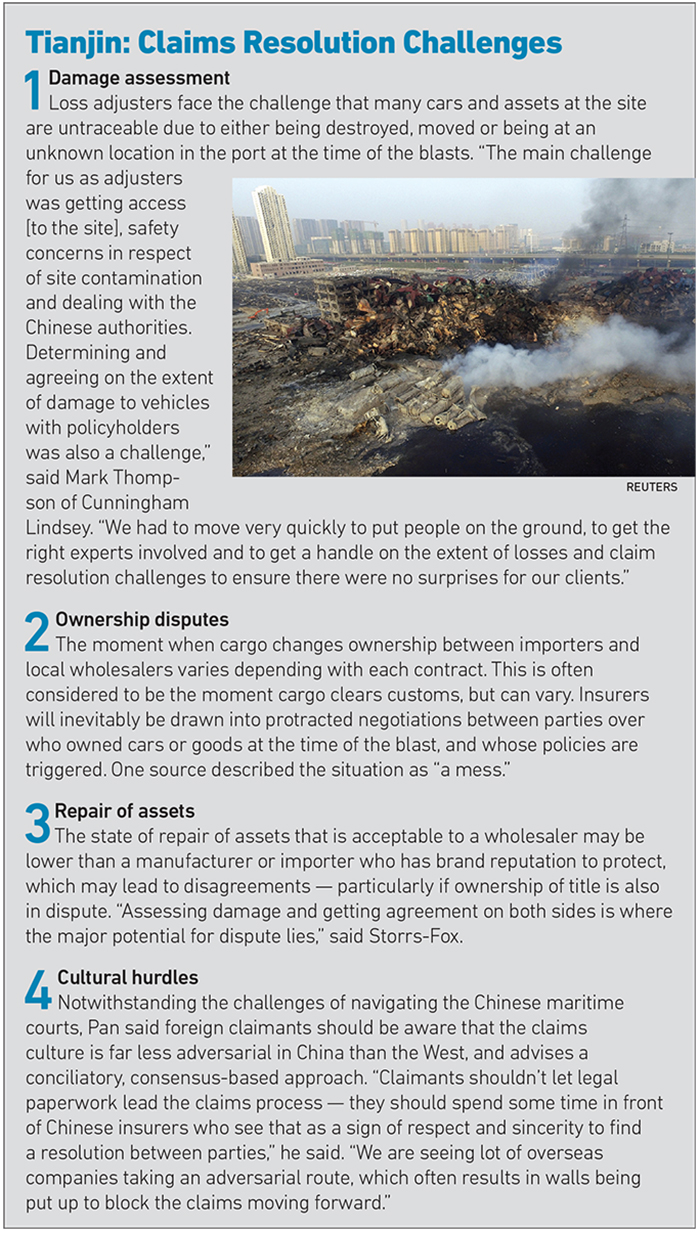

Assessing Tianjin’s Damage

The insurance fallout from last year’s Tianjin Port explosions, which caused nearly 200 deaths and insurance losses that could exceed $3.25 billion, appears as sprawling as the gargantuan Chinese port itself.

Primary liability for the disaster currently sits with Rui Hai International Logistics Co. — the warehouse operator that allegedly stored 3,000 tons of hazardous goods, including 70 times the legal quantity of sodium cyanide in its warehouse, resulting in an explosion equivalent to a 2.9 magnitude earthquake.

However, the chances of affected companies across a multitude of sectors winning compensation from Rui Hai are very slim indeed. One source described the operator’s liability policy as “not worth the paper it’s written on.”

Craig Neame, partner, Holman Fenwick Willan

Not only would the policy be of insufficient value to recover the hundreds of millions of dollars of liabilities unfolding from the event, but the policy is very unlikely to be honored by the insurer if Rui Hai is proved to have flagrantly breached regulations on the storage of dangerous goods.

Rui Hai may not, however, be the only company on the hook.

“There will be a Chinese investigation, and if that concludes there was widespread knowledge and the willful turning of blind eyes, parties who didn’t inform customers their cargo was at risk or take the necessary steps to protect their cargo could potentially be liable,” said Craig Neame, a partner at Holman Fenwick Willan. Class action lawsuits could not be ruled out down the line.

But, said Lincoln Pan, CEO of Willis China, “We’re advising our clients that seeking liability-based damages is going to be tough as it will be very difficult to prove liability and successfully claim against the individuals who may have been at fault.”

Meanwhile, Peregrine Storrs-Fox, risk management director of TT Club (the biggest insurer of containers and cargo at Tianjin) said that Chinese maritime courts are unlikely to accept proceedings until the Chinese government concludes its investigations. “If there is no recovery, due to a lack of recoverable assets or difficulty enforcing a foreign judgment in China, the loss will rest wherever it fell,” he said.

It is more realistic, then, that companies affected by the disaster will have to rely solely on their own insurance policies to recoup any losses — with property, cargo and business interruption policies taking the brunt of the claims. According to Pan, Willis Towers Watson has several clients that suffered losses exceeding $100 million as result of explosion. “These cases will require real advocacy and negotiation to get the fullest type of recovery back from insurers,” he said.

Key Policies Triggered

Damage to buildings in the vicinity of the blast will trigger property and business interruption policies worth up to $1.2 billion, according to Guy Carpenter. The majority are being handled by Chinese insurers, which are reportedly being encouraged by the Insurance Association of China to pay claims promptly and with minimal dispute. Damage to specialist equipment may also trigger covers provided by London and international underwriters, with Swiss Re ($250 million), Hannover Re ($104 million) and XL Group — now XL Catlin — ($100 million) among the highest pre-Christmas loss projections.

Peregrine Storrs-Fox, risk management director, TT Club

Zurich projects $275 million in property and marine losses, but told Risk & Insurance®: “The nature of many of the losses and the extended remediation period to complete repairs mean that uncertainty as to the final cost remains.”

A Lloyd’s market spokesperson said: “We are not clear what the quantum looks like, so it is too soon to tell what the impact on the Lloyd’s market will be. In the coming weeks, we hope to have greater clarity.”

Guy Carpenter estimates that container losses could reach $60 million, while lost or damaged cargo stored at the port could be worth more than $500 million. As many of the manufacturers and importers are international firms, much of these losses will be shouldered in the global insurance markets.

“When car insurers were doing their modelling, I don’t think they considered the risk of an adjacent warehouse storing chemicals in a huge breach of government-imposed regulations.” — Craig Neame, partner, Holman Fenwick Willan

However, Neame said cargo losses may be lower than projected. “There’s been very little reporting into the insurance market of substantial cargo losses, which suggests a lot of the containers were empty — the big loss is the cars,” he said.

According to Guy Carpenter, more than 22,700 cars were destroyed or damaged in the blasts, with a potential loss value of up to $1.5 billion, with many major car firms affected.

While these losses would trigger either cargo or property losses depending on who had ownership of the vehicles in the supply chain at the time, sources believe several manufacturers were inadequately insured.

Lincoln Pan, CEO, Willis China

It is rumored that because of limits on the number of vehicles that can be insured at one location, some manufacturers may not have declared all of their exposed vehicles, and may have to absorb the loss of their unprotected excess assets.

Pan added that certain local importers may also find themselves underinsured, having insured their assets using book value rather than market value.

“Some parties insured just for the manufacturing cost of the inventory, and are now seeking claims on the commercial value. Most insurers are rejecting or contesting these claims.

“Risk managers should analyze the value of their assets as they move through the supply chain, and insurance should be procured according to the maximum potential value of the asset rather than the financial value of an asset in any one point in the supply chain,” he added.

Throw in some large deductibles on the policies that are in place, and it appears that with so many companies having to absorb uninsured losses, the insurance industry may not come out of the event as scathed as it perhaps could have.

The biggest unknown is the impact on supply chain. The port system is now diminished and struggling to cope with the relentless demands of economic trade through China, with logistical disruptions and delays permeating throughout the regional economy.

While this should trigger a host of business interruption (BI) and contingent business interruption (CBI) policies — particularly among international companies — Neame believes there will be substantial uninsured losses when it comes to business interruption as a result of logistical delays rather than physical loss, as this is unlikely to trigger most BI policies. “I suspect the majority of Chinese manufacturers don’t buy CBI,” he added, “though there’s no guarantee CBI would respond either.”

Nick Derreck, chairman of the International Union of Marine Insurers, said in the wake of the event that the accumulation of related risks from the disaster served as a “wake-up call to all cargo insurers,” and called for new technology to help underwriters handle this kind of aggregated risk. Meanwhile, Neame suggests the insurance industry may put tighter limitations on how much stock can be stored in certain locations without the policyholder obtaining assurances on site safety, particularly in developing markets.

Mark Thompson, CEO, Cunningham Lindsey International

“When car insurers were doing their modelling, I don’t think they considered the risk of an adjacent warehouse storing chemicals in a huge breach of government-imposed regulations — this has opened up their eyes to a new type of risk,” he said.

But loss adjuster Mark Thompson, CEO of Cunningham Lindsey International, noted that while some insurers are now coming to terms with “much bigger exposures than they thought,” he doesn’t believe this event will be as damaging to the insurance market’s coffers as recent catastrophes in Thailand or Japan.

While Storrs-Fox said the event is unlikely to lead to any material changes in insurance terms, he advises insurance buyers to ensure they have a “force majeur” clause in their cargo contracts, and also to maintain high levels of due diligence over the practices and procedures of counterparties, including ensuring subcontractors are adequately insured, and operating in compliance with regulations.

It is unlikely the unscrupulous activities at Tianjin are isolated. Both insurers and insureds must learn their lessons from the disaster quickly if they are to avoid similarly complex settlement challenges in the future.